I’m sure you’ve heard by now that the internet was on fire last week, and nearly broke. Yes, there was that Kim Kardashian Paper magazine cover that apparently got a few clicks. But what really set tongues a waggin’ – in payments at least – was the rogue video that went viral of the encounter between Walmart’s Mike Cook and Visa’s Jim McCarthy at an industry conference. The topic of conversation was – surprise, surprise – the cost of payments acceptance. In fact, my guess is that Jim and Mike got more clicks from payments peeps than Kim’s torso. Now that’s an accomplishment.

These two internet-breaking events actually have a lot in common – they’re both marketing plays aimed at furthering a not-too-secret agenda. In the case of Ms. Kardashian, it’s to keep her pop culture brand front and center (it’s really tempting to make a pun here but I’ll refrain). For Mr. Cook, it’s about keeping his gripes about the cost of payments acceptance front and center, too.

The Cook-McCarthy exchange did surface a few new thoughts for me about the central issue that’s at the core of that long-standing merchant-network stand-off. The cost of payments acceptance is obviously important enough to merchants that 60 or so of them joined Cook and Walmart three years ago to establish what some early on coined the “Mike Cook Exchange” – MCX. MCX and its members have poured millions of dollars since then into developing their own payments network; a network that, in theory, would make the cost of accepting a payments product cheaper than it is for them now.

You have to really be mad at the networks to take such a costly and extreme step. But what merchant wouldn’t want cheaper or free anything! When it comes to payments, though, it’ll take decades for any positive impact of this scheme to be felt by the merchants, assuming it gets traction and is successful.

And, assuming it gets out of the starting blocks.

After three years, MCX still doesn’t have a product in the market although it promises one “in early 2015.”

The proposition that it’ll take decades-to-get-any-positive-impact has to do with a couple of key payments realities, starting with the fact that merchants never seem to get rid of any existing payments method, even when new ones are added. And adding MCX/CurrenC into the merchant payments mix would seem to only increase their cost of payments since it isn’t free to build or operate a payments network while they continue to accommodate the preferences of their consumers.

Merchants still take cash and checks even though most people carry plastic mag stripe cards in their leather wallets and have been doing so for decades. Those same merchants will continue to take those mag stripe cards even when CHIP cards are introduced since it’ll take a lot of time before all consumers have CHIP cards and before all merchants have terminals capable of accepting them. And, merchants will continue to accept all of the above even when the method of accessing those payment methods is a mobile app in a store or online.

Merchants will do that for one simple and important reason. They want to accommodate the payments preferences of their customers. And, most consumers want to use different payments methods for different types of purchases in different types of stores. Consumers might prefer to use debit cards when they go to the grocery store, buy sundries at the drug store, goodies at discount retailers, and to pay for their dry cleaning. They might use cash to buy coffee, lunch and afternoon snacks, their REDcard when shopping at Target, their credit cards at the hardware store, and private label cards at their favorite retailers. Some segments of consumers, like the un- and under-banked, disproportionately use cash at all of the stores they visit. And millennials use debit disproportionately everywhere because they don’t likely have access to credit products.

The point here is that until virtually all consumers use the same method of payment in every single store – regardless of whether those methods of payments are accessed by an app or a card in a leather wallet – merchants will continue to support all of them. Well, the ones that they believe any significant chunk of consumers will want to use.

And that’s key.

Merchants have to be convinced that enough consumers have access to that method of payment and will want to use it in their stores. Merchants – who are in the business of selling stuff first and foremost –just don’t want to go the mat over denying consumers the use of their preferred payment method. That’s why cash is still going strong after 3,000 years – it’s something that every consumer has access to and most merchants will always accept – and why merchants accept American Express. It’s also why it’s hard to imagine network-branded cards will go the way of the doo-doo bird at merchants anytime soon – in spite of how much MCX/CurrenC may want that to happen and may spend the better part of three or four decades trying to make happen.

So, until enough transactions flow thru MCX/CurrenC, merchants will spend more on payments by going with this cooperative. They’ll have to invest to support the network, invest in subsidies to persuade consumers to give it a try, and may find that it even likely cannibalizes already low cost payments methods like cash and debit. And, until at least Q4 next year, MCX merchants also need to concern themselves with the exclusivity clauses that prevents them from accepting other popular mobile payments alternatives and the risk that consumers will take their business elsewhere if they happen to like those competing payments schemes and can’t use them.

To me, all of that sounds like a lot of additional risk and cost and I have trouble seeing how MCX is going to provide merchants with a good return on their investment or really reduce transactions costs that much. .

But that doesn’t mean that merchants are stuck without options or are entirely dependent upon MCX to be successful to skinny down their payments acceptance costs. There are a few things that merchants can do right this very minute. Many of these options have been available to merchants for a very long time.

So, here you go.

Insist That Consumers Use Cash

I’m really not being cute.

If merchants really, really, really do have an issue with how much it costs to accept credit cards, they should do more to encourage consumers to use plain old cash. They could give them incentives to use cash, install ATMs to make it easier to use cash, and tell consumers that using cash will get them lower prices. My nail salon does that (but I still use my debit card), The Heart Attack Grill in Vegas, the 2nd Street Café in Cambridge MA and Charlie Benlich’s in Chicago does too.

Now private ATMs have fees that might turn consumers off. But there’s a way around that. Merchants can leverage the ATMs that offset their fees via advertising. Not only will advertisers get a new channel to access consumers, consumers will be able to use out of network ATMs for free and not get stuck picking up the tab for the fees that merchants don’t want to pay.

Of course, consumers will have to be persuaded to do this since consumers don’t really care (or even know) how much it costs merchants to accept card products. It will have to be made worth their while to take the extra step to stop at the ATM machine on their way to checking out. (Unless someone invents an ATM machine that just gives cash to the consumer at the checkout!) That means that merchants will have to actually plow their interchange fee savings into funding benefits to the consumers that, be okay that their consumers are still invisible to them when they use cash and be convinced that accepting cash and incenting consumers to use it is a more cost effective solution all the way around. In a mobile world, that may take extra convincing. But maybe things like lower prices on products, express lanes for cash customers or other goodies could be enough for some consumers to make the switch, since all consumers have access to cash.

Surcharge Consumers Who Want To Use Credit Cards

As part of the networks’ settlement with merchants and the Justice Department over merchant rules, merchants are able to surcharge consumers using cards. Well, sort of. The technicality here is that American Express opted out of the settlement and is excluded from the ruling, and therefore the surcharge provision. So this technicality means that the ~3 million merchants that don’t take American Express cards today can add an additional fee to purchases consumers make with network branded credit cards right now. Merchants that accept American Express cards can also decide today, to ditch them, and earn the right to surcharge, too.

Mind you, I haven’t seen anyone do this except for a taxi scheme which adds a $3.00 convenience fee for paying with a credit card (all of you who just left Vegas paid that fee if you used a taxi). Of course merchants have been able to offer cash discounts for a long time but aside from gas stations hardly anyone does that either.

But, if everything’s on the table, this is an option available to merchants today who are interested in covering the costs associated with accepting cards and who aren’t worried that consumers will wonder why they’re being charged extra for using a card at a store that has never done so in the past.

Channel Their Inner Starbucks

Merchants can do what the most successful mobile payments scheme in the US has done and create a scheme that puts a merchant-branded reloadable stored value card in between a funding source like a debit card and checkout. That reduces the cost of payments for merchants by reducing swipe fees to a single swipe fee when the card is loaded/reloaded and by giving merchants, in theory, the use of the funds on the card until they are spent.

Now this gets a little dicey since the current MCX contractual provisions say that theirs is the only mobile payments apps that member merchants can accept. But the MCX CEO said publicly that there are no penalties for merchants who want to get out of their contracts. For any member who might want to exercise that option, or any non-member who might wish to explore this option, there are innovators in the business of making these schemes possible for merchants, including one whose team includes the guy who created the Starbucks app!

Of course, the challenge will be to get consumers to partition money off in individual merchant stored value accounts for use at a future point in time. That works for Starbucks since it involves $15 or $25 at a time and at a store that consumers visit daily and leverages a loyalty benefit that consumers value. But with the right incentive, perhaps consumers would be motivated to transfer a few hundred bucks at a clip into a Whole Foods branded card, to use over the course of the month when they shop there.

Call LevelUp

For merchants with concerns over the cost of payments, LevelUp’s Interchange Zero mantra should sound like music to their ears. LevelUp’s been around for a couple of years and has 14k merchants and something like 2 million consumers signed onto its platform and is going geography by geography to get density, just like Facebook did with it ignited.

Today, merchants can sign on to the LevelUp branded and/or white label version of their app and, not exactly pay zero, but deploy a mobile loyalty wrapped around payments application that’s said to drive all kinds of incremental value to merchants at a much lower cost of acceptance.

Like the Starbucks’ scheme, LevelUp keeps the cost of payments low in a number of ways – aggregating purchases and swipe fees, persuading consumers to attach debit and not credit cards to the app (most do, they say) and driving more frequent visits to merchants because consumers get benefits (cash back when spending thresholds are met) when they do. The QSR/convenience store merchant, which is where LevelUp has established its presence, also gets the benefit of knowing who its cash only or card only customers are when they use the app, and can market to them on a regular basis which increases incremental sales at those merchants.

Implement PayPal And Steer Customers To ACH

PayPal has had a 15 year head start in creating a consumer brand proposition rooted in safe transacting online and now, using an app and/or digital account to pay in app and in some stores. To the great distress of the issuers and networks, over the years, they have strongly encouraged consumers to attach their checking accounts and not credit card accounts to those accounts when transacting. Last year, PayPal also announced that its “wallet” would also accommodate private label cards, which drives the bread and butter/crème de the crème spending of a merchant’s customer base.

In store, PayPal’s deal with Discover enables it to connect to the physical point of sale via the Discover network. And, yes, while that’s never as easy as it sounds, it’s no more a slog than what everyone else trying to get accepted at the physical point of sale is going thru now.

Now, again, consumers would have to be incented to use PayPal at the physical point of sale and to do it using their checking accounts or private label cards, but there’s an existing base of consumers to start with and incent – private label cardholders and the 187M existing PayPal account holders. And, presumably a high degree of merchant interest to juice that incentive if reducing the cost of payments acceptance is, indeed, top of their minds.

Channel Target’s REDCard

No one really knows what the CurrenC product will be but we hear that it will involve ACH and CurrenC branded accounts linked to a consumer’s checking account. I understand why that’s attractive to merchants. The Target REDCard drives more than 20 percent of Target’s volume and Target claims that REDCard customers spend 50 percent more than other customers and visit the store twice as often. The REDCard hook is the cash back incentive that made it possible for those consumers to feel more than okay giving up their checking account credentials to Target. Naturally, Target loves this program for the positive impact to its overall economics.

The breach has put a bit of crimp in that program and since then, Target has turned to MasterCard to issue an EMV version of the product. I presume that deal includes favorable rates to Target, but was also an essential move to keep REDCard consumers in the REDCard boat post-breach.

CurrentC is hoping that it can replicate that program’s success for every single merchant that’s part of its network. But network-branded ACH/decoupled debit products aren’t new and don’t need CurrenC to make happen. In fact, the concept’s been around since 2002 when Debitman launched with 100k merchants. (Who out there remembers Debitman? In addition to being a decoupled card network, it was the only card product with its own theme song and superhero logo. It was renamed Tempo.) Merchants have had this option available to them for more than a decade and can create decoupled card programs today as long as they’re able to incent consumers to hand over their checking account credentials in order to establish an account. Admittedly, that could be a bit trickier in the age of the merchant breach.

But there are all sorts of schemes now in the market that are all about accommodating any merchant that wants to do that. In addition to PayPal as mentioned previously, Zipline aka National Payment Card, Paydiant (the platform powering CurrenC) and Seamless are but three players that are helping merchants develop and deploy ACH/merchant-branded mobile schemes.

Incent Consumers To Use Debit Cards

Durbin essentially put a price cap on debit products in 2012 and reduced the cost of debit card acceptance by 40 percent. It’s not zero or as low as what the merchants were hoping to get but it’s pretty darn cheap to process debit payments now. Further, merchants get the option to route their debit payments to the cheapest set of rails available to them.

Issuers have stopped offering rewards for the use of debit products given the lousy economics associated with those products for them, but there’s nothing to stop merchants from plowing their interchange savings into incentives to sway consumers to select debit and not credit at checkout. And, if merchants chose to do this via some of the third party mobile apps that are swirling around, I’ll be that they might even persuade them to pony up a few basis points to subsidize usage.

The tricky part here is persuading consumers who’d like the benefit of credit when making higher dollar purchases or who like getting credit card rewards or who don’t want feel comfortable using debit products online or in a mobile app to switch. That means that the incentive will have to be rich enough to get consumers to be comfortable making that tradeoff.

Double Down On Private Label Cards

Now that the economy is recovering, unemployment is down and consumers are back to work and shopping a bit more, more merchants could, in fact, decide to take the plunge and administer their own private label programs. That would require giving consumers incentives to get them on board and merchants working with a good partner that can manage the credit risk associated with those programs, but it’s another option available to merchants right now.

Private label cards are, of course, humungous drivers of profit to merchants even though they’re a tiny part of the overall card mix for consumers. Where they work well, they’re used by the brands’ most loyal customers. Neiman Marcus’s twenty year old InCircle program, for instance, drives 40 percent of the company’s sales – even though it accounts for a small fraction of its overall customers. And since, the average APR on these cards is higher, in fact as much as 8 points higher than the national average for general purpose credit cards these loyal customers pay higher fees if they revolve their balances.

The trick is making the incentive rich enough for consumers to both open an account and use it repeatedly, not just the first time it’s offered to get the 20 percent off savings. And, of course, making sure that credit worthy consumers opt-in.

Now many of you reading this are probably wondering – is Karen being really helpful here or is she being sarcastic? The answer is maybe a little of both.

Merchants have a lot of options available to them today – and have had them available – if priority number one is reducing the cost of accepting payments. But most haven’t explored some of these options, presumably because they’ve done the mental math and concluded that it isn’t worth messing up their relationship with the consumer over the hassle of asking them to switch from a payments method that they like to use to an other one that may be more of a hassle and less appealing. Then again, maybe others are now more attractive now since the mobile payments landscape is becoming more clear.

Merchants have a lot of options available to them today – and have had them available – if priority number one is reducing the cost of accepting payments. But most haven’t explored some of these options, presumably because they’ve done the mental math and concluded that it isn’t worth messing up their relationship with the consumer over the hassle of asking them to switch from a payments method that they like to use to an other one that may be more of a hassle and less appealing. Then again, maybe others are now more attractive now since the mobile payments landscape is becoming more clear.

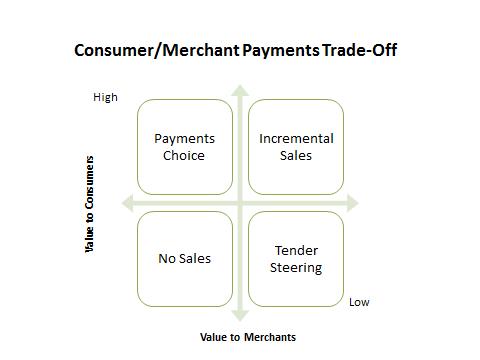

This suggests that what the merchant dialogue over the cost of payments acceptance should be all about is putting the cost of payments into the context of value to consumers and value back to them. And, that would seem to be about creating a solution that gets consumers and merchants into the upper right quadrant of my 2×2 matrix –incremental sales.

And, that seems less about the looking at the pure cost of payments and more about how merchants can now use the new tools they have available to them to get more consumers to buy more stuff in their stores.

When that tool was solely point of sale acceptance via the convenience of using a plastic card, the options available to merchants were somewhat limited, often expensive and cumbersome for them to deploy and difficult for consumers to find and use. But in the age of mobile and the cloud and data, that’s all different now. There are oodles of new ways to access the consumer, understand her preferences and drive value back to her in a way that delivers the promise that lives in the upper right hand quadrant.

Naturally, how these tools are used and third parties they partner with will vary based on the merchant, and their willingness to consider different options and use incentives to get consumers on board. But the notion that the only way this can be done is by steering consumers to a different underlying method of payment that’s cheaper for the merchant and offered by a consortia of competing merchants who I don’t think will ever comingle their data and whose MO is mostly about creating cheaper rails seems, today, as much of a fairy tale as it was when I originally wrote about it three years ago.

Because, as I just pointed out, if cheaper payments acceptance was the only end game, there are many ways to skin that cat – yesterday, today, and tomorrow.

Which is why I don’t think that’s what merchants really have as their number one priority.

I think that priority number one is selling more stuff and letting consumers use the method of payment they feel most comfortable using. Look at ShopRunner. Its American Express customer acquisition strategy is about having consumers register those cards to ShopRunner accounts for use throughout its merchant network. American Express isn’t exactly the cheapest form of payments there is. But ShopRunner merchants are happy to accept ShopRunner accounts linked to American Express because that’s the payment method those customers want to use, and those customers end up spendingmore with them, and go on to become newcustomers at other ShopRunner merchants.

Incremental sales trumps the cost of payments acceptance every time.

That’s not to say that there isn’t work to be done or discussions to be had on the cost of payments, especially as we enter this new world of mobile-enabled payments, on and off line. At the risk of sounding like payments Pollyanna, it seems like now is the time for merchants and networks and third party innovators to have a constructive dialogue over the new mobile-enabled point of sale economics. It does seem confusing today and even a bit ambiguous as some mobile schemes get better rates than others even though they all use tokens and mobile phones and apps. But it’s early days, and there’s a lot for everyone to both learn and consider.

Wouldn’t it be nice if we could do that with everyone’s eyes focused on the value delivered across the ecosystem and not just costs of transacting in a mobile payments world.