Unless you have been hiding under a rock, you know Oct. 1, 2015, was the deadline for the “liability shift.” After Oct. 1, the party that caused a non-EMV transaction to occur (i.e., either the non-EMV card issuer or the merchant that does not have an EMV-compatible POS system) will be the one held financially liable for any resulting counterfeit fraud losses.

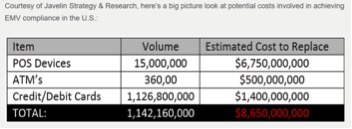

The move to chip-based EMV cards has created a $1.4 billion opportunity in just card manufacturing, according to Javelin Strategy & Research. Somebody has to make all those replacement cards, after all!

The main U.S. company trying to grab this $1.4 billion prize is CPI Card Group (PMTS), which went public last Friday (Oct. 9) with a market cap of around $900 million.

CPI Card Group

Depending on your perspective on digital wallets, CPI Card Group is either a great “pick-and-shovel” investment in the non-cash payments system or the last buggy whip manufacturer!

According to its prospectus, CPI Card Group:

- Issued 360+ million cards in 2014, representing about 35 percent of the market (making it #1 in the U.S.)

- Provided card services to over 3,200 card-issuing banks and prepaid debit card issuers

- Serves over 4,000 customers, including JPMorgan Chase, Bank of America, American Express, Wells Fargo, InComm, Green Dot and Blackhawk Network, as well as thousands of independent community banks, credit unions, group service providers and card processors.

If you are interested in payments, you will want to read the prospectus as it is chock-full of interesting details about the overall payments market. I found these items especially interesting:

Advertisement: Scroll to Continue

- According to the prospectus, “EMV cards may sell for five to 10 times the average selling price of the magnetic stripe cards they are replacing. We estimate based on our experience that the industry-wide average selling prices per card, exclusive of services, are approximately as follows: magnetic stripe — $0.20 per card; Contact EMV — $1.00 per card; and Dual-Interface EMV — $2.00 per card. Comparing our costs to selling prices, we achieve similar gross margin percentages across these three card types [my emphasis added].” Similar gross margin percentages across all three is good for those of you who want to invest. I always wondered what the cards cost!

- “The Nilson Report estimates that card-based payments have increased from 38.3 percent of U.S. transactions in 2005 to 56.5 percent in 2013, and electronic payments have increased from 4.3 percent to 7.2 percent over the same period. By 2018, card-based payments are projected to comprise 69.2 percent of U.S. transactions, with cash and checks accounting for 21.4 percent and electronic payments representing the remaining 9.4 percent. We believe that this long-term trend of card-based and electronic payments replacing cash and checks will continue.” CPI Card Group is trying to convince you the “buggy whip” in this market is cash, not cards, and that digital forms of payment will get more hype than market share for the foreseeable future! (That seems likely!)

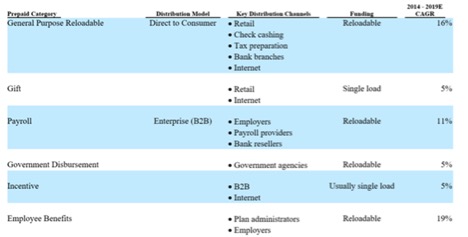

- Growth in bank debit cards is expected to be less than 2 percent annually. Growth in general purpose credit cards is expected to be 4 percent annually. The fastest-growing market segment is prepaid debit cards, which are expected to grow 8 percent annually. In other words, our wallets are full, as expected.

- Within the prepaid market, the segments driving growth are new uses, not gift cards:

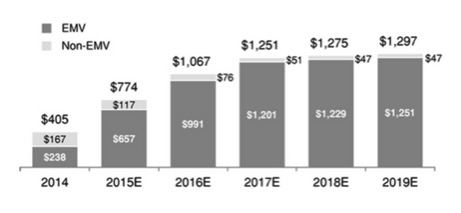

- The big excitement is reserved for the EMV replacement market, which CPI Card Group sees sustaining the company for a long while as these two charts demonstrate:

Summary

I’m not going to opine on whether this is a good investment or not — I’d be wrong in any case. But it is fascinating that pedestrian aspects of the payments system, like the card manufacturing, can provide insights into the overall payments market. For CPI Card Group, clearly, the future is still one word: plastics!