Talk about poking a hornet’s nest.

MPD Founder and economist, David Evans, wrote a piece on Friday about Apple Pay that got a lot of people talking. In it, Evans basically said that he was ready to make a call on Apple Pay and much earlier than he thought.

Here’s what he said.

“Apple Pay is fizzling. And unless it drastically changes course, Apple Pay will follow the hundreds of other attempts, made around the world in the last seven years, that have sputtered along at low levels of use or, much more frequently, have just flat-out died.”

Evans’ Apple Pay verdict was fueled by data that came out of a survey done by InfoScout of 400 Apple Pay users on Black Friday. That data showed that the early adopters of Apple Pay, well, aren’t really adopting. Only 10 percent of all iPhone 6 users have ever tried to use the mobile payments method. And those who could use it – so had iPhone 6’s and were in stores that could accept it – weren’t using it either. Only 4.5 percent of those who could have used Apple Pay actually did.

As you can imagine, Evans’ conclusion generated a lot of comments and discussion on and offline. I thought I’d summarize the major points of debate that surfaced as comments on his piece, as talk around the water cooler, and all over Twitter and add a bit more context, fact base and counterarguments so that we can keep this important conversation alive.

Imagine a start-up knocking on the door of a merchant asking them to enable a new form of payment. The incentive they dangle is the prospect that 6 out of every 1000 consumers walking into their store would be capable of using this new method, based on the results of an initial beta test, a pretty committed set of stakeholders, and massive consumer advertising by those stakeholders as part of the beta test.

Many of the comments to Evans’ piece, as well as the piece PYMNTS published on Monday interpreting the InfoScout survey results was that it was totally idiotic to call Apple Pay a disappointment after only 60 days.

But the start-up scenario that I just described is the reality of Apple Pay today.

Yes, it’s true that it’s early days.

But here’s where the early day Apple Pay “exit poll” results raise a few cautionary red flags.

The people with iPhone 6’s/6 Plus’ in their mitts right now are the early iPhone adopters. These are the guys and gals who rush to get the latest Apple gadgetry no matter what and try it all. But despite the big Apple Pay sales pitch by Tim Cook at launch, it doesn’t seem that those early adopters were all that interested to try Apple Pay. I was actually surprised that the number of iPhone 6 users who ever tried Apple Pay was only 10 percent – I thought it would be a lot higher.

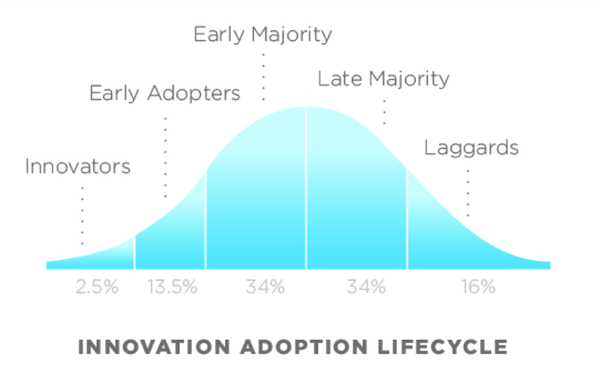

The famous Rogers Diffusion of Innovation Bell Curve spells out the importance/worry associated with Apple Pay’s low usage. Early adopters are pretty important to getting innovation off the ground. It’s their enthusiasm for and adoption of new products or services that reduces the anxiety of others to give it a try. They may be a small percentage of the overall population, but they’re a vitally important part of any ignition strategy.

In the case of Apple Pay, the issue comes down to this: the early adopters aren’t adopting Apple Pay even after the initial hype and promotion and aren’t using it every chance they get. If I were Apple Pay, I’d be worried.

And, I’d be worried, because with adoption that low from the early adopter crowd, the march across the chasm to the early and late majority could be a long and slow crawl.

One that makes for some pretty challenging ROI calculations for the merchants who are essential to the ignition of Apple Pay and who need to be convinced that turning on NFC is going to deliver one of two things for them: incremental sales or the loss of sales they already have if they don’t.

Join me at the virtual white board here while we walk thru the ROI analysis of Apple Pay today. These calculations run you thru the funnel of people in the US with smartphones, those with iPhones, those with iPhone 6’s and 6 Plus’, those who want to and who have used Apple Pay.

| Percent of U.S. Shoppers Using Apple Pay | 2014Source: PYMNTS.com | December 2014 | |

| 2014 sales of iPhones Globally Apple has not reported this number but has said this is what they expect and it appears they are on track, at least this is what analyst say. 80M represents the high end of the range |

80,000,000 |

| US Share of iPhonesIt’s been reported that iOS shares in the US approximates 44 percent | 0.44 |

| iPhone 6s in US in 2014 | 35,200,000 |

| Adults in the US ages 18-65 | 197,896,653 |

| iPhone 6 Users in the US.Here’s where we are extrapolating data. iPhone 6’s aren’t selling as well in the US as they are in other parts of the world, so we are not assuming a 44 percent share. We are assuming 30% of 80 million sold have been sold in US. This number, by the way, is consistent with other estimates of iPhone 6 sales in the US. | 24,000,000 |

| Apple Pay Stats for 2014 | |

| Fraction who turn on Apple Pay (from InfoScout survey) | 10% |

| Users with Apple Pay | 2,400,000 |

| Percent of shoppers with Apple PayThis is the number of all shoppers with Apple Pay – which is 12 out of every 1000 shoppers. It is 2,400,000 divided by the number of adults in the U.S. | 1.21% |

| Fraction of iPhone 6 users who use Apple Pay (from InfoScout – we rounded 4.5 percent up to 5 percent) | 5% |

| Users who use Apple Pay | 1,200,000 |

| Percent of shoppers who use Apple PayThis turns out to be 6 out of every 1000. | 0.61% |

The bottom line is that only 6 out of every 1000 consumers who walk into a store will likely use Apple Pay, provided of course that they are in a store that accepts it, which means that the merchant has NFC.

And, this is where the calculations get even a bit more troubling.

At the moment, only 220k merchant locations are enabled with Apple Pay – which represents less than 150 merchants in total, many of them grocery. Large accepting merchants like McDonalds account for ~17k locations of that 220k.

So when you further adjust the 6 out of every 1000 that could use Apple Pay by the small number of merchants that enable Apple Pay today – so the possible places that Apple Pay users could actually use it – the volume of spend driven by Apple Pay starts to look miniscule and the business case for merchants enabling it starts to look really tough and potentially unconvincing.

Apple Pay’s strategy was to get banks and networks on board initially, and only 24 out of 8 million merchants ( 100 more grocery store merchants were brought on board later). At the risk of ticking off my issuer friends, what Apple Pay needed a whole lot more than the banks early on were the merchants. Consumers would have registered their cards to their Apple Pay accounts in a New York minute if they had lots of places to use them – just like they did when they enabled their Starbucks accounts, PayPal accounts, LevelUp accounts, Visa Checkout and MasterPass accounts. None of whom needed issuer cooperation or endorsement to launch their mobile payments application.

In that case, issuers would have had to do what issuers have always had to do – make sure that the cards consumers registered to Apple Pay was theirs. But Apple Pay would have had lots more places for their consumers to use their accounts and the ability for those consumers to develop an Apple Pay payments habit at those merchants – which would have given more merchants more of a reason to sign on too.

“Adoption has been slow given consumer’s reluctance to embrace the change.”

This is a quote from the UK Payments Council Report last year on the state of contactless/NFC payments in the UK – a country that has been held out as the poster child for NFC ignition.

Evans mused in his piece whether Apple Pay’s inability to set the mobile payments world on fire could be chalked up to what he described as “the NFC curse.”

He said “A decade of failed attempts to get NFC-based contactless cards off the ground, and now half a decade of failed attempts to get NFC-based mobile payments off the ground, should convince us that, whatever the merits of this technology is, it is a loser from the standpoint of igniting mobile payments.”

NFC is a payments POS solution that seems to have been looking for a willing consumer population to inspire an unenthusiastic merchant population to adopt and ignite it now for a very long time. In the UK, according to the UK Payments Council, outside of transit and transportation, usage is sparse, in spite of the fact that there are loads of contactless cards in the marketplace and where most merchants have installed contactless POS terminals. The UK Card’s Council reported in August 2014 that a transaction milestone of ~698M transactions in retail setting, of which 37M were identified as being NFC/contactless (this excludes all transit and transportation). That’s about a 5 percent penetration at the POS. And, 37 percent of those transactions were under 10£, mostly concentrated in food/coffee/QSR.

And in Canada, where 75 percent of the merchants enable contactless, and have for a while, only 10 percent of transactions are contactless. In an article that suggested that Apple Pay should have launched in Canada and not the US given its large concentration of contactless-ready merchants, an analyst from Gartner said that while contactless cards and merchant acceptance was more established in Canada that didn’t mean that NFC mobile would have a “head start” there. “[Mobile] NFC needs to show it brings more value than contactless cards for people to switch. So I still expect a slow start for NFC in Canada,” she was quoted as saying.

The few countries that have mobile NFC aren’t doing any better. South Korea is another NFC/contactless success story that people talk about shows a similar result. Only about 6 percent of POS transactions are mobile/NFC according to MasterCard’s Index, despite 97 percent of the population owning a mobile phone.

The two lowest common denominators for using mobile payments in a store are consumers having a mobile phone and an app that enables a payment to happen with a POS system. That’s why the most successful in-store mobile payments schemes so far have been those that enable payments via any mobile device – like mPesa – and via the cloud on any mobile device – like Starbucks, PayPal, Dunkin’ Donuts and LevelUp.

The iPod was introduced in October of 2001 about 9 months after the iTunes store launched. As those of us who were Sony Walkman owners back in the day know well, iPod wasn’t the first MP3 player in the market. It was, however, the first really cool, small and elegant one that provided access to a vast library of music that could be purchased a song at a time from the iTunes store.

However, when the iPod launched, consumers could use the device to load songs from anywhere, including ripping CDs, onto those iPods, even though the process was admittedly a bit clunky. We’ve been reminded of this fact recently since we’re all reliving the history of the iPod courtesy of the big antitrust case now being played out in court. The topic of iPod and music access was part of Eddy Cue, Apple’s Head of Internet Software and Services, testimony just last week.

Cue was quoted as saying, “You could take the songs you bought in another store and burn them onto a CD and then rip them back into any device or music player you wanted.”

That makes the Apple Pay and the iPod go to market scenarios starkly different. As Evans would say, you guys are applying one-sided logic to a two-sided world.

Apple’s always been about giving people their own devices to access to a variety of solutions right from the start. It’s un-Apple for Apple to launch a solution that imposes such severe constraints on both sides of its addressable market. For instance, making Apple Pay only available at a small number of merchants that are NFC enabled and via special devices that only a small subset of consumers will own – isn’t a page out of the Apple ecosystem ignition playbook. Or a sure-fire way to crack the chicken and egg problem in a two-sided ecosystem like payments that requires scale.

Apple has typically ignited new things by letting others do the hard work for them. Apple’s ignition playbook is to seed an ecosystem by giving innovators access to the hundreds of millions of consumers already on its platform, its hardware and operating system assets and the ability to have their innovation reach those consumers efficiently. That recipe for ignition allows Apple to push the “problem” of scale out to the innovators who are given lots of tools and incentives and creativity to create the solutions that appeal to the Apple device owners.

But Apple Pay is different. It requires that merchants and consumers both invest in and adopt a technology that merchants and consumers don’t have in the U.S. (and a critical mass of either won’t for a long time) and that both have pushed back on in most all other parts of the world. That kinda puts a damper on getting innovators excited to play along.

And getting merchants to jump into the Apple Pay fray will take a bit of work. The Apple ecosystem is but one set of customers that merchants will want to accommodate. Decisions on their part will have to consider what’s likely to be the technology that the majority of consumers across any mobile operating system will have and be capable of using over the long term. It’s one of the reasons there’s been such pushback on NFC for so many years. And, the experience so far with Apple Pay may not have done much to change that sentiment.

It’s true that economics is a profession dubbed by many as the “dismal science, and that Evans has more than once lived up to his reputation of being a dismal scientist. But he also wrote that he took no great pleasure in calling Apple Pay a fizzle and made the call not because he was feeling cranky but because he’s seen this movie before in many other payments and platform-based ecosystems, having worked with a number of the key players in those ecosystems over the years.

Both of us wrote in separate pieces the day that Apple Pay was launched of Apple’s great opportunity and our great hope for it to energize and ignite the mobile payments ecosystem. We thought that its powerful brand, it’s easy and frictionless way to provision cards to the Apple Pay wallet, its unique and valuable tokenization scheme to assuage the security concerns of consumers, and its expertise in assembling and igniting ecosystems would finally move us all closer to the mobile payments reality that holds such fabulous potential for every player in the ecosystem. We also independently wrote that it may have also been the catalyst to ignite NFC-enabled mobile payments. .

So, it’s profoundly disappointing that Apple Pay, given its profile, it stakeholders and its ecosystem hasn’t done more to live up to the hype and create the mobile payments groundswell that we all seek.

But it’s also not surprising. Igniting two-sided ecosystems is hard. And, since payments is a multi-sided ecosystem, it’s especially hard. It requires a really keen understanding of how they work in the first place and then what it takes to get them to ignite. It also means knowing how to make the most critical decision of all – knowing which side of platform is critical to get on board, and then givng that side the right incentive to get them on board. It also requires a candid look at why others have failed, and in payments, why those very few experiments with respect to mobile payments and commerce have succeeded and what’s made the few success stories successful. .

Those characteristics are as simple to describe as they are hard to execute. Mobile payments needs to solve a problem that a critical mass of people have. In developed economies, moving people from a system that works everywhere means that a key stakeholder better give people a really compelling reason to switch and lots and lots of places to use it once they’ve been incented to give it a try.

That means that any one of the players in this ecosystem can help to solve Apple Pay’s ignition problem. The networks could solve this problem for Apple today by giving merchants an incentive to install NFC terminals right now (just like they did when debit was introduced). Issuers could work with the networks to enable super-duper card linked offers at those merchants to give consumers more reasons to use their cards in those Apple Pay wallets at those NFC-enabled merchants. Apple could give more merchants a reason to care more by plowing some of the money they’re getting from the issuers into merchant-specific promotions so that they might be incented to promote Apple Pay to their customers.

Apple could also decide to re-read its own ignition playbook and ditch its technology-centric approach to v.1 of Apple Pay and move to the cloud. It could mobilize beacons and Apple Pay and all iPhone users and incent the boatload of innovators with ideas to do what they’ve always done – develop apps that give iPhone toting consumers lots of cool new reasons to enable and use them.

But it seems that one thing is clear so far. This time won’t be different just because it’s Apple. Even Apple can’t rewrite the rules of platform ignition.

{kind=link}