Money mobility has become a top priority for consumers continuing their journey into a more connected economy. Beyond frictionless moving funds from accounts, mobility now has come to include instant access to deposits made with common payment options such as cash, check, real-time payments and credit cards. For FinTech issuers working in consumer-facing products hoping to steal share from traditional banks, this ability has quickly gone from a “nice to have” tool to a mandatory offering. However, consumer confidence in sector FinTechs to provide services on a par with traditional financial institutions (FIs) is equally necessary.

PYMNTS has found that FinTech issuers overall have some catching up to do. In particular, those considered lower-performing need to go a long way before they may fully compete with their more established competitors. For the ongoing “Money Mobility” collaboration with Ingo Money, PYMNTS has focused on tracking FinTechs working in consumer-facing payment products or services as well as finance and financial operations generating revenues of $5 million or above annually. Within those parameters, the Money Mobility Index was calculated using metrics contributing to customer satisfaction. A higher Index score represents a greater chance of an issuer gaining new customers and providing them with the money mobility tools they seek. Analyzing both money-in and money-out transaction features, PYMNTS has found that the typical FinTech account issuer scores an average Index rating of 53.5 out of 100. The 30 issuers with the lowest Index scores averaged just 35.6 as an Index score.

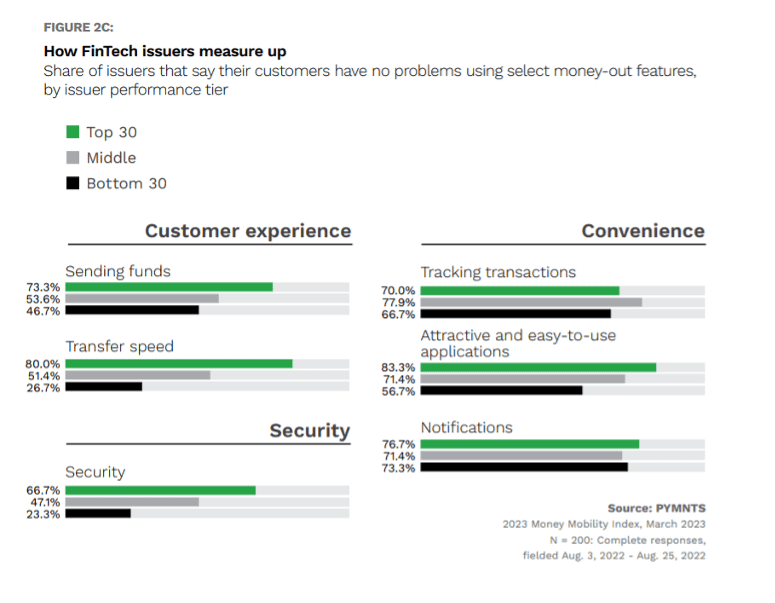

The latest in this series, “2023 Money Mobility Index,” finds that these bottom performers lag far behind their higher-performing peers when it comes to money-out security.

More than three-quarters of these FinTech issuers say their customers have issues with money-out security. Among the leaders, only one-third report these difficulties. Such a large gap when it comes to security satisfaction from better-performing sector competitors would be concerning at any time. However, in today’s digital banking world, consumers value security over convenience, meaning this inadequacy could spark a customer exodus in search of issuers providing better data protection.

In an interview with PYMNTS’ Karen Webster, Ingo Money CEO Drew Edwards explains how part of the problem may lie in the piecemeal strategy some FinTech issuers take. “They’re stitching stuff together, one partner at a time, one vendor a time, and I think that’s a mistake, because of fraud. If you can’t see the whole picture, then it’s hard to control the bad actors. It’s really hard to offer great customer experiences and control the risk at the same time.”

The ray of hope for these bottom-performers looking to catch up may be that with some focused effort, there could be room for improvement. However, without such attempts, it may be only a matter of time before customers move on to safer pastures.