Despite efforts to influence consumers to use electronic forms of payment, such as debit and credit cards, cash remains the top payment instrument consumers use to pay, especially for small-value transactions, according to a recent Fed report. Mobile-based payments, however, barely scratch the surface.

Companies that specialize in cash-based services, such as ATM deployers, have been saying for some time that cash use is not going away any time soon. A recent Federal Reserve report appears to back up those claims.

In fact, consumers choose to use cash over any other payment form, including debit and credit cards, according to the Fed report. “Evidence from the Diary of Consumer Payment Choice.”

“Cash plays a dominant role for small-value transactions, is the leading payment instrument for many types of purchases, and stands as the key alternative when other options are not available,” the report notes. “In certain cases, including that of mostly lower-income consumers who lack access to alternative payment options or find them too costly or difficult to obtain, cash is also used for relatively larger-value transactions.”

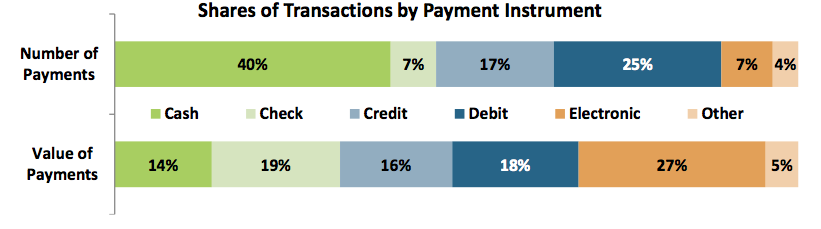

In October 2012, the average American consumer conducted 59 purchases and bill payments, and 23 of the payments, or 39 percent, involved cash. Debit cards accounted for 25 percent and credit cards 17 percent. Electronic methods, such as online banking bill pay and automated clearinghouse payments, accounted for 7 percent, the same percentage as checks, according to the report.

“All other payments represent less than 5 percent of monthly transaction activity, with text and mobile payments barely registering at less than one half of one percent,” the authors noted.

Use of payment types changes, however, when comparing by transaction amount (see chart). Cash accounted for a relatively small share of total consumer transaction activity at 14 percent, while electronic methods make up 27 percent and checks 19 percent.

“These findings suggest that, although consumers don’t use electronic methods or checks very often, when they do, it tends to be for much higher-value transactions,” the report noted “In contrast, cash is used quite often, but primarily for low-value transactions. In fact, the average value of a cash transaction is only $21, compared with $168 for checks and $44 for debit cards.”

Earlier this month, a Bankrate.com report suggested that, because consumers carry so little cash with them, it wouldn’t take longer for a cashless society to form. However, earlier reports pointed the trends headed in a different direction.

In March, Market Platform Dynamics CEO Karen Webster spoke with Steve Rathgaber, CEO of ATM owner and manager Cardtronics Inc., in a podcast interview. “I think between now and 2020, we’re in pretty good shape,” Rathgaber said, after citing recent cash-use trends.

Later that month, a study from Balance Innovations suggested that, with rising cash use, merchants should do more to manage their cash to keep their cash-handling costs down. “Many consumers like to use cash because it’s anonymous and carries little risk, but for retailers it can be very time consuming to manage and reconcile,” Shelley Bosler, Balance Innovations senior vice president for strategic initiatives, said in the survey findings announcement. “Increased usage of cash among consumers makes it all the more important for retailers to optimize cash processing policies at both the corporate and store levels.”

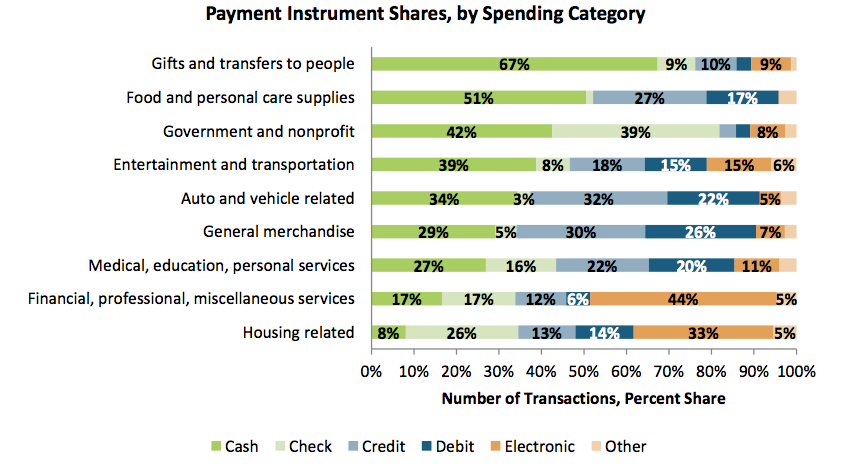

According to the Fed report, cash is the leading payment instrument for several expenditure categories, including gifts and other transfers between individuals; food and personal care supplies; entertainment and transportation; medical, educational, and personal services; and government and nonprofit expenditures (see chart). It is the second most frequently used payment instrument for all other categories except housing, and a distant second for financial and professional services.

“The average ticket size for many of these expenditure categories is relatively low, suggesting that the reason cash is the most or second-most frequently used payment instrument is because small-value transactions tend to dominate these categories,” the report’s authors noted. “Moreover, the fact that debit cards tend to be used frequently for these expenditures as well indicates that cash usage likely is not the result of a lack of access to alternative payment options.”

Indeed, when looking at payment preferences, debit card use stands on top. About 43 percent of consumers deemed the debit card as their payment instrument of choice, and that’s consistent with the fact those same consumers use their debit card for the largest share of all their transactions. Similarly, when considering the 30 percent of consumers who prefer cash and the 22 percent who prefer credit cards, both use their preferred payment instrument for at least half of their transactions, the Fed’s research found.

“Checks, however, are an anomaly,” the report noted. “The 3 percent of consumers who prefer checks actually use cash twice as often as they use checks. This may reflect subtle (and not so subtle) social pressures to use a faster alternative to the check for the point-of-sale transactions that make up a large share of consumers’ everyday expenditures.”

Looking to future potential changes in cash use relative to other payment instruments, the Fed said it will continue its work to understand how the continued growth of debit cards, the expansion of prepaid cards among the unbanked, and novel P2P solutions may influence how consumers use cash, and the potential effects on the Fed’s cash business.