The mass manufacture and distribution of vaccines means the pandemic will eventually come to a close, but its effects on the payments industry could very well be felt for years to come. Social distancing and stay-at-home orders have driven in-person retail shopping and consumer banking online, and the increased volume in online payments has become a golden opportunity for money launderers. The ongoing economic downturn has also given these criminals more chances to carry out their schemes, with many exploiting stimulus payments, insolvency relief plans and credit restructuring to move money around without alerting authorities.

The mass manufacture and distribution of vaccines means the pandemic will eventually come to a close, but its effects on the payments industry could very well be felt for years to come. Social distancing and stay-at-home orders have driven in-person retail shopping and consumer banking online, and the increased volume in online payments has become a golden opportunity for money launderers. The ongoing economic downturn has also given these criminals more chances to carry out their schemes, with many exploiting stimulus payments, insolvency relief plans and credit restructuring to move money around without alerting authorities.

Banks and payment providers have been scrambling to make sense of the new digital normal as it pertains to money laundering and anti-money laundering (AML) initiatives. Many AML programs’ existing flaws have been amplified by this increased volume, with time-consuming manual processes, poor-quality data and changing regulatory expectations becoming the top frustrations AML staff reported last year.

Banks and payment providers have been scrambling to make sense of the new digital normal as it pertains to money laundering and anti-money laundering (AML) initiatives. Many AML programs’ existing flaws have been amplified by this increased volume, with time-consuming manual processes, poor-quality data and changing regulatory expectations becoming the top frustrations AML staff reported last year.

The April “AML/KYC Tracker®” explores the latest in AML and know your customer (KYC) developments, including the growing problem of money laundering during the pandemic, how money launderers are changing their tactics and why some AML teams view the increased payments volume as a prime opportunity to gain more AML data than ever before.

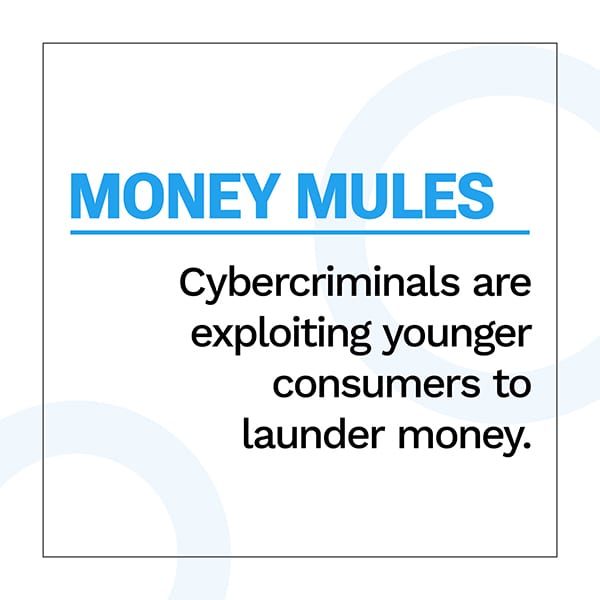

Money launderers have been increasingly targeting younger bank customers in their schemes, with consumers ages 21 to 30 becoming their prime targets. A recent study found that victims from this age group accounted for more than 40 percent of money mules last year, a 5 percent increase from 2019. Fraudsters typically exploit health crisis-related economic anxieties by offering potential mules a cut of the transferred funds, but they are dishonest about what they plan to use the funds for and often threaten violence against those who try to back out of these schemes.

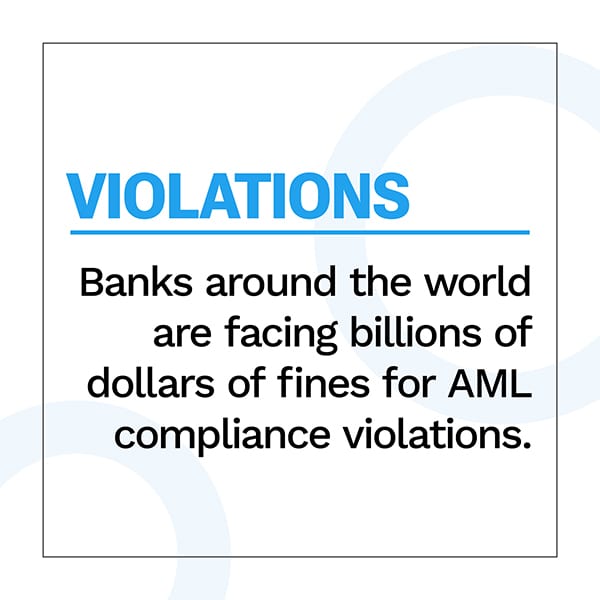

Oversight agencies are cracking down on banks with substandard AML procedures, with more than $6.8 billion in compliance violation fines issued to 28 financial institutions (FIs) across 14 countries in 2020. The largest single penalty was given to Australian bank Westpac, which was fined $900 million for its failure to report more than 19 million cross-border transactions over numerous years. Authorities said that some of these payments were allegedly linked to human trafficking operations in the Philippines.

Oversight agencies are cracking down on banks with substandard AML procedures, with more than $6.8 billion in compliance violation fines issued to 28 financial institutions (FIs) across 14 countries in 2020. The largest single penalty was given to Australian bank Westpac, which was fined $900 million for its failure to report more than 19 million cross-border transactions over numerous years. Authorities said that some of these payments were allegedly linked to human trafficking operations in the Philippines.

The record-setting compliance total in 2020 could be a drop in the bucket compared to 2021, however. Oversight agencies in the United States imposed $200 million in fines in just the first two months of 2021, putting the year on pace to top 2020 by a wide margin. Most of the new fines are the result of the Anti-Money Laundering Act (AML Act) of 2020, which builds upon the Bank Secrecy Act of 1970 to include antiques dealers and virtual currency marketplaces and also gives law enforcement new tools to crack down on money laundering.

For more on these stories and other AML and KYC headlines, download this month’s Tracker.

Money laundering has stepped up in volume during the pandemic alongside the growing number of digital payments, furnishing AML teams with plenty of data to help them train their cybersecurity models. Many experts have focused too closely on money laundering itself rather than its underlying causes, however.

In this month’s Feature Story, PYMNTS spoke with Max von Both, senior vice president of compliance at payments provider Paysafe, about why cybersecurity teams must fight fraud and money laundering together using real-time transaction analysis.

In this month’s Feature Story, PYMNTS spoke with Max von Both, senior vice president of compliance at payments provider Paysafe, about why cybersecurity teams must fight fraud and money laundering together using real-time transaction analysis.

Money launderers have dramatically altered their tactics in light of the pandemic’s new digital paradigm, keeping AML staff on their toes. Economic insecurities and increased digital banking activities have provided ample opportunities for money launderers to launch their schemes, and stay-at-home orders have made AML and KYC procedures even more difficult to complete.

This month’s Deep Dive explores how money launderers are taking advantage of pandemic-related uncertainty and anxiety as well as how AML and KYC teams have reacted to these new circumstances.

The “AML/KYC Tracker®,” a PYMNTS and Trulioo collaboration, provides an in-depth examination of current efforts to stop money laundering, fight fraud and improve customer identity authentication in the financial services space.