From Australia, the land that invented buy now, pay later (BNPL) as we now know it, comes news this week that laws are changing to treat the installment payment product as credit.

The move may well make its way around the world in much the same way BNPL itself has.

Addressing the Responsible Lending and Borrowing Summit in Sydney Monday (May 22), Australia’s Assistant Treasurer and Minister for Financial Services Stephen Jones said “the government will change the law, so that buy now, pay later products are regulated as credit products.”

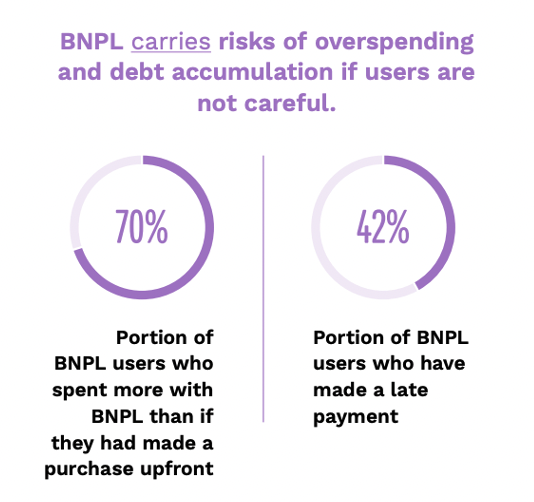

Citing a litany of issues reported to the Australian Securities and Investments Commission (ASIC) that add up to “unacceptable levels of unaffordable lending occurring, largely concentrated amongst low-income borrowers,” Jones said, “BNPL looks like credit, it acts like credit, it carries the risks of credit.”

Promising draft legislation in the coming months and the introduction of a final bill to the Australian Parliament by the end of this year, Jones said regulatory changes will include the need for BNPL issuers to hold Australian Credit Licenses; that they comply with Responsible Lending Obligations; meet statutory dispute resolution and hardship requirements; comply with statutory product disclosure and other information obligations; abide by existing restrictions on unacceptable marketing; and meet a range of other minimum standards concerning their conduct and about their products.

This is the latest and most definitive set of measures yet proposed among nations where BNPL is under increasing regulatory scrutiny, and it’s unlikely to be the last. United Kingdom Economic Secretary to the Treasury Andrew Griffith MP has been outspoken on the need to regulate BNPL. In a February consultation paper titled “Regulation of Buy Now, Pay Later,” the U.K.’s Financial Conduct Authority (FCA) asked for input on the matter by April 11.

The UK has differentiated short-term interest-free credit (STIFC) loans from BNPL and is drafting legislation granting the FCA new enforcement powers to address what it deems irresponsible or misleading BNPL marketing and issuance, primarily among FintTechs and merchants.

Getting ahead of the regulatory changes, BNPL giant Klarna announced in a press release Wednesday (May 24) that it has “launched the U.K.’s first voluntary credit ‘opt-out,’ an additional tool in the Klarna app to help consumers save time, money and worry. The new feature will help consumers achieve their financial goals by providing them with a tool where they can ‘pre-decide’ not to use credit, perhaps while saving for a specific life event or sticking to a very strict budget.”

The idea “was initially suggested by Andrew Griffith MP, U.K. economic secretary to the treasury in a meeting” with Klarna CEO and Co-founder Sebastian Siemiatkowski.

Meanwhile, rumblings of similar moves to come continue in the United States. The Consumer Financial Protection Bureau (CFPB) began looking into BNPL in 2021, and in March of this year released a study of BNPL use, noting that “While many BNPL borrowers who we observed used the product without any noticeable indications of financial stress… They are more likely to also have traditional credit products like credit and retail cards, personal loans and student loans…”

They are also more likely to exhibit measures of financial distress than non-users, the study found.

CFPB Director Rohit Chopra said in a September letter outlining the bureau’s BNPL fact-finding mission: “Because they are deeply embedded as a payment mechanism for eCommerce, buy now, pay later lenders can gather extraordinarily detailed information about your purchase behavior in a way traditional cards cannot.”

“Buy now, pay later has mimicked parts of Big Tech’s surveillance model to harvest and monetize data in ways that banks and credit unions have typically avoided,” Chopra said in the letter. “Many of these firms have created their own gateways and digital, app-driven marketplaces, powered by personalized behavioral data, to lure their users into buying more products financed through a buy now, pay later loan.”

The April edition of PYMNTS’ “Buy Now, Pay Later Tracker®,” a collaboration with Splitit, noted that BNPL has operated “largely free of government oversight since its launch, following in the footsteps of many of its counterparts in the tech world. Much like ridesharing, streaming media subscriptions or short-term property rentals, the BNPL market surged while governments debated how — and if — the market should be regulated. This laissez-faire environment could quickly be drawing to a close, however, as governments across the globe consider regulations that would apply many of their existing credit laws to the BNPL market.”

The April edition of PYMNTS’ “Buy Now, Pay Later Tracker®,” a collaboration with Splitit, noted that BNPL has operated “largely free of government oversight since its launch, following in the footsteps of many of its counterparts in the tech world. Much like ridesharing, streaming media subscriptions or short-term property rentals, the BNPL market surged while governments debated how — and if — the market should be regulated. This laissez-faire environment could quickly be drawing to a close, however, as governments across the globe consider regulations that would apply many of their existing credit laws to the BNPL market.”

Splitit Chief Legal and Risk Officer Omri Flicker said: “The credit card regulatory regime makes a lot of sense, and [Splitit is] trying to stay within that regime. There are a lot of consumer protections there, and so we think the interest in BNPL by regulators should be welcomed.”