It’s the end of September, summer’s a distant memory, and students are only a few weeks into settling into the routine of books, homework, and given the way things are going …

… paying for it all.

You’d be forgiven for thinking the conversation around what we might term “education affordability” has been confined to student loans, and specifically, to the resumption of student loan repayments.

And, indeed, as has been well-documented in this space, the fact that the repayments are now coming back in full force means that borrowers now stand to lose a significant percentage of their discretionary income.

But there’s another leg to the discussion of affordability — namely, paying for education while it’s ongoing.

And against the backdrop of high interest rates, and the fact that loan repayments stretch out over decades, it may be no surprise that other financing options are gaining a wider embrace — and a closer look on the part of regulators.

As reported this month, the Consumer Financial Protection Bureau (CFPB) has published a report on tuition payment plans, is in the midst of collecting more information, and has warned about fee structures and, in some cases, inconsistent disclosures.

In the report, titled “Tuition Payment Plans in Higher Education,” the bureau noted that “almost all payment plans observed by the CFPB are structured to cover a student’s tuition and other expenses for a single academic term (e.g., semester or quarter) and typically require borrowers to pay off their outstanding balance in three to six installments.” The CFPB also reported that it “recently estimated, based on newly available data, that private sector lending for education by BNPL lenders increased by 1,028% between 2019 and 2021.”

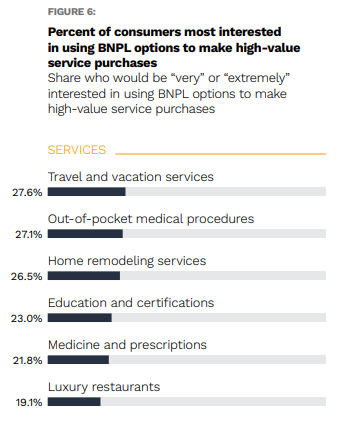

The families considering the trade-offs between installments and more traditional lending conduits are in effect weighing funding education with (in part, at least) the available cash on hand vs. the decades-long, after-the-fact obligation that private and federal loans demand. And in the 2021 report, “The Next BNPL Horizon: Expanding Access To High-Value Services,” done in collaboration between PYMNTS and AWS, we found that nearly a quarter of consumers would be “very or extremely interested” in using BNPL for education, as shown in the chart.

More recently, in the report “The Automated Campus: Enabling the Future of Higher Education,” with joint efforts between PYMNTS and American Express, the significant opportunity for schools to interact with students in ways to cement payment plans and educate them on options is considerable, as 67% of students say that managing payments — and making them — are among the most important features.

There have been a number of announcements spotlighting the use of technology to streamline and improve the payments process, especially in an international setting, where complexity reigns and multiple currencies might be involved.

In one example, from this summer, Flutterwave’s Tuition offering will enable African users to conveniently pay fees to educational institutions both within Africa and overseas by using their local currencies.

Elsewhere, Flywire and Tencent Financial Technology said they were working together to leverage digital wallet Weixin Pay (WeChat Pay) to enable international payments. Flywire, for its part, said this week that in general, adoption of installment plans is significant if those plans are on offer. Eighty percent of students, the company has said, indicated that the option to pay for their education in installments would enable them to “better afford” their education expenses.