Inflation is proving a tough beast to tame.

Data from the U.S. Department of Labor released Thursday (Oct. 13) showed that consumer inflation’s growth rate eased just a bit — but not by much.

The Consumer Price Index (CPI) rose by 8.2% from last year, down slightly from the 8.3% gain seen in August.

The core CPI, which strips out the ever-volatile impact of energy and food, was up 6.6% in September, which is the fastest pace in 40 years. And for the U.S. consumer, triaging bills now has become commonplace and is a juggling act that cuts across all segments of the economy.

About 60% of us live paycheck to paycheck, with little left in the till once the monthly nut is covered. The latest report on the new reality confronting the peer-to-peer (P2P) consumer shows that there’s a widespread reconsideration of expenses — what’s essential, what’s not.

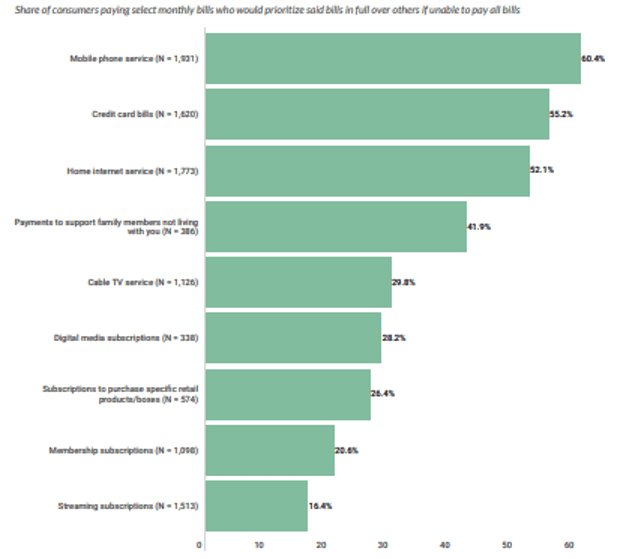

Juggling the Bills

The juggling act will only intensify, and if the Federal Reserve keeps hiking rates in a bid to blunt inflation’s rise, there will be the additional burden that takes shape when debt becomes more expensive.

But even under unprecedented pressure, consumers value credit and do not want to risk falling behind on their credit card debt.

PYMNTS research revealed that consumers would prioritize mobile phones and credit card bills over other expenses. Sixty percent would prioritize their phones, and 55% would put credit cards at the top of the list.

And while the data pointed to the fact that mobile phones are the lifeline for all manner activities, credit is the lifeline that helps pay other expenses, particularly as the savings we built during the pandemic have started to dwindle.

PYMNTS data from earlier this year showed that the savings for people who live paycheck to paycheck but do not have issues paying their bills have dipped to a bit more than $6,800, down from more than $8,300 at the peak. For the paycheck-to-paycheck consumers struggling with expenses, the average stands at less than $3,000, down from more than $4,000.

Thus, credit becomes more essential than it might have been in a long time.

We’ll know more in the next few days as to just how consumers are maintaining and meeting their monthly payment obligations tied to their cards. Earnings season is just beginning, and as soon as Friday (Oct. 14), J.P. Morgan, Citi and others will weigh in on card balances, loan loss reserves and delinquency rates.