Card disputes have long been viewed as a necessary evil in retail banking and commerce — a cost center to be managed and minimized. But new research from PYMNTS Intelligence and Banyan, “How Card Disputes Are an Opportunity to Cultivate Customer Loyalty,” reveals that these friction points actually represent critical moments that can either cement or destroy customer loyalty.

Here are three data points to consider when rethinking how both merchants and card issuers think about disputes:

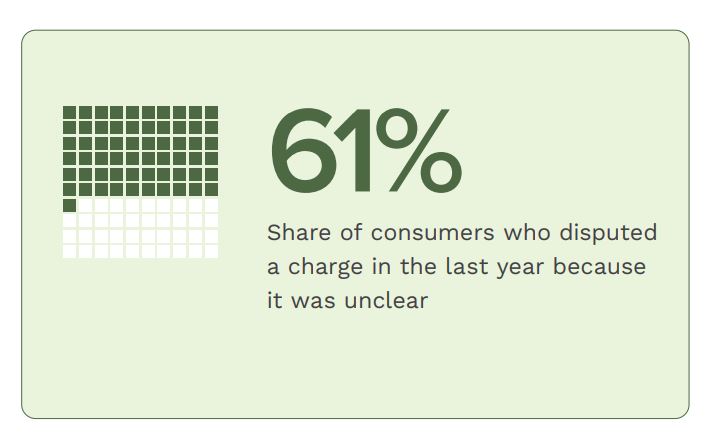

While the payments industry has invested heavily in fraud prevention, the data shows that confusion — not criminal activity — is actually driving most disputes. A remarkable 61% of consumers initiated disputes simply because they didn’t recognize or understand charges on their statements. This led to higher dissatisfaction rates (29%) compared to actual fraud disputes (12%).

While the payments industry has invested heavily in fraud prevention, the data shows that confusion — not criminal activity — is actually driving most disputes. A remarkable 61% of consumers initiated disputes simply because they didn’t recognize or understand charges on their statements. This led to higher dissatisfaction rates (29%) compared to actual fraud disputes (12%).

The takeaway? The industry’s intense focus on fraud prevention, while important, may be overshadowing an even more fundamental need: clear merchant identification and transparent charge communication. Simple improvements in how charges appear on statements could prevent many disputes before they begin.

When it comes to handling disputes, speed isn’t just about operational efficiency — it’s about keeping customers. The research found that 52% of satisfied consumers cited fast processing as a key factor in their satisfaction, while 50% highlighted the importance of accessible customer service.

The stakes are particularly high for maintaining relationships with frequent card users. Among this valuable segment, 86% said they were likely to continue using cards that efficiently handled their disputes. The message is clear: Investing in rapid dispute resolution capabilities isn’t just about reducing back-end costs but protecting future revenue streams.

Perhaps most surprisingly, the research reveals that disputes don’t just impact the card issuer-customer relationship — they put merchant relationships at risk, too. One in four cardholders who disputed a charge stopped shopping at the merchant where the purchase was made.

This impact shows generational variation, with 41% of baby boomers and seniors saying a dispute negatively impacted their likelihood of returning to a merchant, compared to just 11% of Gen Z consumers. The data suggests that older consumers tend to have higher spending power and are particularly sensitive to dispute experiences.

According to PYMNTS Intelligence, these findings suggest that the industry must fundamentally rethink its dispute approach. Rather than treating them solely as a risk management challenge, disputes represent critical moments of truth in customer relationships.

For merchants, this means investing in clearer payment identification and front-line dispute resolution capabilities. For card issuers, it means treating dispute resolution speed as a competitive differentiator rather than just an operational metric. And for both, it means recognizing that every dispute represents not just a potential loss to be managed but an opportunity to strengthen — or weaken — customer loyalty.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More