![]()

—

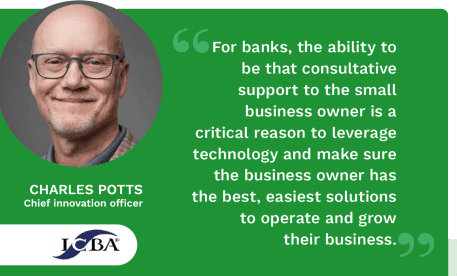

For his role with the ICBA, Potts works closely with community banks to ensure they are staying ahead of the technology curve and doing everything they can to meet customer needs and stay competitive. Potts said nearly two-thirds of all small business loans come from the community banking industry, illustrating the close, symbiotic relationship they have enjoyed over the years. Together, they represent an enormous and vital swath of our economy, and it is essential their relationship continues to be fruitful, he said.

For his role with the ICBA, Potts works closely with community banks to ensure they are staying ahead of the technology curve and doing everything they can to meet customer needs and stay competitive. Potts said nearly two-thirds of all small business loans come from the community banking industry, illustrating the close, symbiotic relationship they have enjoyed over the years. Together, they represent an enormous and vital swath of our economy, and it is essential their relationship continues to be fruitful, he said.

The pandemic highlighted and accelerated the very close coupling of community banks and SMBs — most notably around the Paycheck Protection Plan rollout — as well as the growing consumer demand for digital experiences that deliver convenience and speed. Potts encourages community banks to leverage the knowledge, experience and lessons learned from the pandemic when aiming to provide SMBs with the digital tools they need to match those that have been so successful on the consumer side.

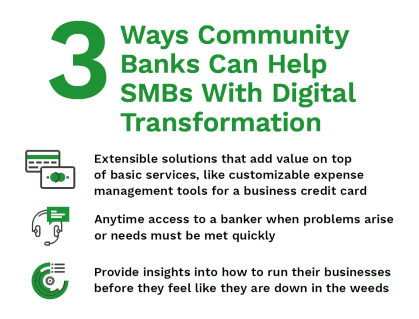

FinTechs and solution providers that introduced winning tech for consumers over the last few years are retooling to provide SMBs with the same capabilities. This digital presence should stretch from marketing, prospecting and processing to origination and onboarding, according to Potts. SMBs need the best solutions available to run their businesses, he said, and on average they are running 15 applications to make that happen. Banks must play a bigger role in smoothing out frictions and suggesting more comprehensive or integrative tools.

Another key for FIs is to understand their customer segments and how different products suit different verticals. Choosing the right technology is a vital step in the process, but FIs too often are unable to fully reap its benefits — or misfire completely, he said. Community banks have typically deferred to their primary technology provider, but with the rapid evolution of technologies like software-as-a-service, cloud-based and mobile-first solutions, digital transformation has proven elusive for many banks relying on traditional tech providers.

With tens of thousands of FinTechs knocking on bankers’ doors, it is often impossible to know what solutions fit best. This led Potts and ICBA to create the ICBA ThinkTECH Accelerator to help community banks access disruptive financial technologies. The 12-week program helps arm community banking teams with cutting edge tools and FinTech entrepreneurs with mentorship and direct connections to ICBA members.

FIs such as Rockland Trust and Agility Bank have been able to access Agent IQ, a ThinkTECH alumni company that offers a digital platform driven by artificial intelligence (AI) that improves communication among banks and their customers, for example. Through Agent IQ, Rockland Trust’s personal and business customers can digitally access a banker within minutes via its YourBanker product, and Agility Bank built a technology stack to find the right vendors to meet clients’ needs.

Entering its fifth year, the accelerator program has been so popular and impactful that ICBA hired staff to run the accelerator in-house. Potts said the goal is to provide year-round programming that is more granular to address customer challenges with digital solutions, including those that can help SMBs stay competitive.