There’s no doubt that Apple Pay has a lot going for it. It’s the payment method birthed by a beloved consumer brand and technology giant, it has the backing of the biggest payments players on the planet and it has those same players using their own marketing dollars to build consumer excitement and promote it. As a new entrant to payments, it doesn’t get much better than that.

As it’s been described, it also seems to have a lot to offer consumers. Its payments security protocols – biometrics + tokenization – sound reassuringly safe to a consumer population that’s becoming increasingly unnerved by the prospects of their accounts – and identity – being attacked at any time. And activitating Apple Pay accounts couldn’t be easier given the slick card provisioning protocols that have been put in place. But perhaps most important, the reported release date of the iOS version supporting Apple Pay, October 20th, is on the 5th anniversary of the launch of PYMNTS.com so it also has lots of good karma going for it. Thanks Apple, I’m sure that timing was intentional! J

But despite all of the positives, there are some headwinds that Apple Pay will have to overcome, and quickly, in order to ignite and become a credible global payments player. I’ve covered much of this before at a high level in my previous posts. Today I wanted to drill into two that I think are particularly important.

Last week, PYMNTS published a chart in The Apple Pay Ecosystem Tracker (#ApplePayTracker) that made the case for why the world is, as the headline reported, “gaga” over Apple Pay. The iPhone is owned by the most affluent and well educated consumers in the U.S.. Although Apple may only have a 42 percent share of the market there, its owners control about two-thirds of the spend in a market that is finally showing signs of recovery from the 2008 financial meltdown.

But those wealthy consumers have all the credit and debit cards they’d ever want. The habits and preferences that support their use are also pretty well engrained. For those consumers, Apple Pay really won’t change what payment card they use and is pretty unlikley to shift share from one issuer to another. It’s not a coincidence, though, that all of the top issuers jumped on board on day one. Issuers want to mitigate that risk, even though slight, that those valuable consumers will bail on them because Apple Pay is available as a digital payments method. Hold that thought for a minute, I’ll be back to it.

These are also consumers who probably don’t use much cash. When they visit a Starbucks, they’re probably using their mobile app or their debit card to buy those double whipped mocha lattes. The opportunity to flip cash-using customers to digital payments is probably pretty marginal. Apple Pay isn’t likely then to drive incremental volume to issuers.

Merchants are hoping that consumers love using Apple Pay so much that they prefer shopping at their store because the merchants have it available. I know that’s my behavior – having a Starbucks or LevelUp app on my phone really does incent me to seek out those places first when I’m looking for coffee or lunch. When Whole Foods turns on Apple Pay (BTW, those VeriFone terminals are in Whole Foods now just waiting to be used), it might make it harder for me to want to divide my shopping between Whole Foods and Stop N’ Shop for groceries, lack of Chobani yogurt at Whole Foods notwithstanding. The thought of that behavior by other iPhone-toting grocery shoppers could also be enough to cause Stop N’ Shop to seriously consider Apple Pay, too, and, of course, what Apple Pay and the networks and issuers hope for as well. And that’s how its always worked in payments. A few merchants in a category start taking a payment method and everyone follows so as not to lose sales to their competitors.

If the consumer experience is as good as it is reported to be, Apple Pay acceptance, like mag stripe cards 40 or 50 years ago, could become a real advantage to those merchants who offer it and cause entire merchant categories to flip in order to neutralize the “Apple Pay” effect. Of course, getting consumers to spend more and profess their undying love for those merchants beyond that is all a function of making Apple Pay about more than just payments.

And that’s where you gotta believe iBeacons will soon ride the Apple Pay draft. As I’ve said before, for Apple Pay to be successful long term, it will have to be more than just a way to pay for something in a physical store. In app, it will also have to offer consumers with existing digital payments accounts something more than payment to get them to switch. One of the disadvantages that Apple Pay faces now is that it’s not available as an online payments method. In an omnichannel world, consumers might find it awkward that Apple Pay isn’t available across all of the channels they shop.

But for merchants and issuers to really benefit from the “Apple Pay” effect, three other things have to happen. The availability of Apple Pay has to cause certain merchant categories that drive high frequency debit/cash transactions to flip to digital. That means flipping a segment of the population that uses cash to pay for goods and services. It also means making sure that consumers that use a plastic debit card today at those stores, and not cash, are comfortable putting their debit cards into the Apple Pay app.

There are a couple of relevant points to be made here.

Let’s start with getting consumers who use debit cards today to become comfortable sticking them in the Apple Pay mobile app. I’ve heard from some issuers that the best thing about mobile payments (from their standpoint) is that consumers don’t stick their debit cards into the mobile app out of concerns over security and the fear that, in the case of a breach, their bank accounts would be drained.

I’ve heard just the opposite from some mobile apps players so the story here is mixed and obviously a function of the use cases and demographics of the mobile apps users. But taking Whole Foods and grocery as an example, the friction here for any mobile app to overcome, and Apple Pay in particular, is getting consumers to feel comfortable enough to do one of two things: put their debit cards into the app, which is probably what they use to pay today at Whole Foods, and/or being okay with changing their payment behavior to using credit when they are used to using debit.

I’m sure that all of you reading this likely do that anyway to max out your points and because you have the income and discipline to pay off that card balance at the end of the month. And many of the affluent iPhone users are probably that profile, too. But that still doesn’t mean that they’ll do it. It’s a big shift in behavior to “charge” groceries and it remains to be seen if consumers – affluent or not – will do it.

That, of course, suggests that consumers must be comfortable putting their debit cards into a mobile app for Apple Pay to get those Whole Foods transactions. We don’t have enough data to know one way or the other whether consumers will be comfortable doing that. The Fed Survey published in May of 2014 says that the majority of consumers surveyed in 2013 used debit (52 percent) and not credit (42 percent) when using their phones to pay. That was obviously before the well-publicized breaches and when there really weren’t that many mobile payments apps being used anywhere – PayPal and Starbucks were probably the only two at that time with any momentum. I’m not so sure that consumers will feel all that comfortable putting their debit cards into Apple Pay. I’m not saying that they shouldn’t – only that they won’t. Given the nervousness now around data breaches and cyber attacks, we’ll have to see where the consumer nets out. Issuers, of course, would prefer credit transactions as it puts more money in their wallets, but merchants, especially in thin margin categories like grocery, certainly won’t like it all that much.

Let’s move to cash.

When it comes to converting primarly cash-centric customers to digital, we have a whole different scenario to consider. Those customers are disproportionately lower income people and disproportionately don’t have debit or credit cards. They are also a lot more likely to own an Android or maybe even a feature phone. Walmart said it isn’t interested in Apple Pay because it’s supporting its own merchant-centric card scheme, CurrentC. There’s another reason. Its consumer base is lower income, uses a ton of cash in its stores and is a predominantly Android-centric customer. The same holds true for discount retailers like the Dollar Store, convenience chains like 7 Eleven and fast food joints like McDonalds (even though they are an Apple Pay launch partner). For everyone in the payments ecosystem system to really benefit from making transactions digital, it’s the Android users they’ll have to get on board.

Speaking of Android, as I wrote last week, Apple Pay launched first in the U.S. for a very good reason: it has a critical mass of consumers with iPhones and a payments system with a business model that allows it to be monetized. That’s far from the case in every other part of the world. For Apple to be a real global player in payments, it will have to get acceptance all over the world. That will require a rethink of its business model and acquiring a critical base of consumers in those markets.

It has taken a few important steps in that diretion. Apple Pay does leverage a global standard for transacting–contactless EMV and tokenization–which gives it a great head start for playing on a global stage.

But then it hits a pretty big brick wall.

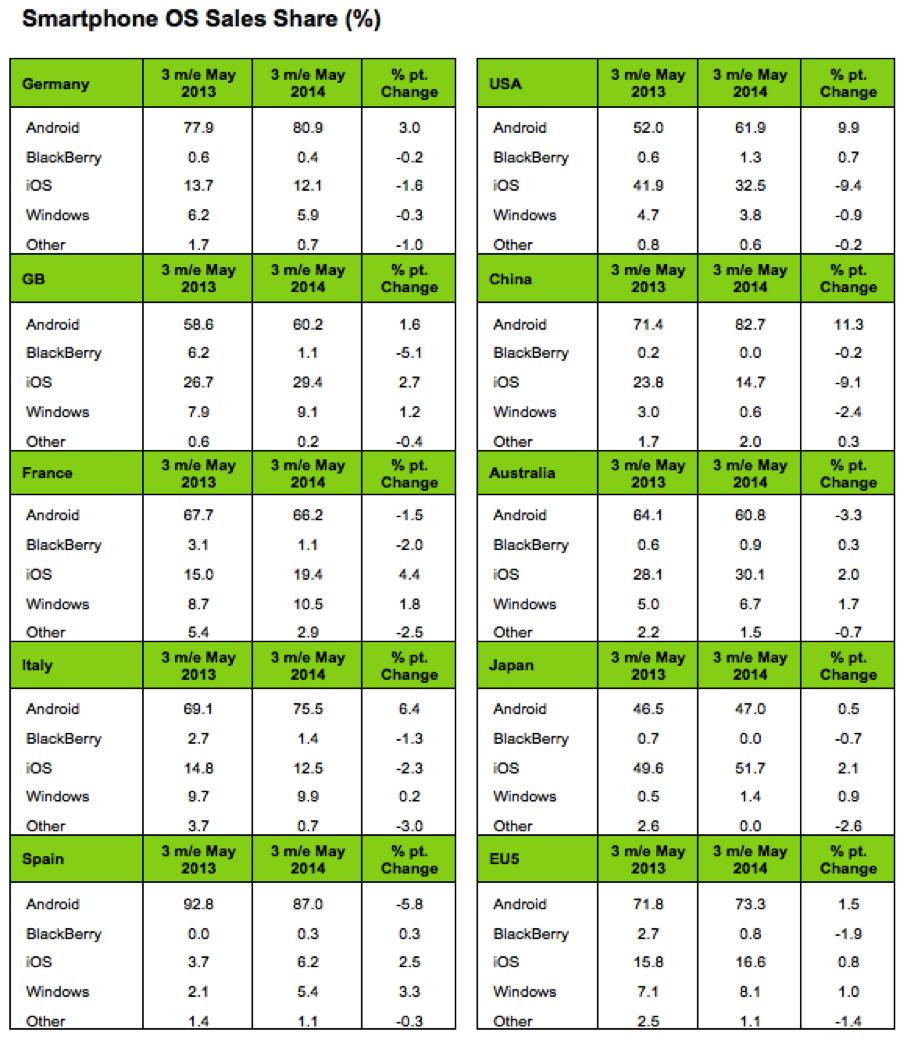

Take a look at this chart as complied by KantarWorldpanel Comtech in May of 2014.

Apple is in a world of hurt just about everywhere else in the world. It’s market share is sub-20 percent in most countries. In China, despite reports that iPhone 6 sales are strong, Apple has a 14 percent share.

That’s not great news for a couple of reasons.

First, the hoopla over Apple Pay and payments gives others with a critical mass of users–Android in Europe and China–a free ride to amp up their own payments capabilties. Take the UK where NFC terminals are just about everywhere. Android has a 60 percent share of the market to Apple’s 30 percent share–the highest of any country in Europe. Getting a critical mass of consumers to use Apple Pay, which will get merchants to care, requires that the banks and networks support it, as they do here in the U.S..

That’s Apple’s second problem.

In Europe, interchange is next to nothing in several sizeable countries and going to probably be next to nothing if the regulators have their way (20 basis points for debit and 30 basis points for credit). It’s unlikely that issuers, who will get hardly anything when their cards are used, will be willing to pay Apple anything like the fees it is getting from U.S. issuers. Apple will just have to be happy selling iPhones and making money some other way. It’s hard to see Apple Pay generating the same sort of excitement from European issuers.

In China, Apple Pay has a few other headwinds facing it.

One is the other 800M digital account gorilla called Alipay. Chinese consumers love Alipay and use it all of the time. Jack Ma and Co. have done a great job of giving consumers all sorts of places and reasons to use it and, as a result, Alipay is very sticky. Chinese consumers can use Alipay to shop on Alibaba, pay their bills, pay for taxis, buy movie tickets, shop in physical stores and now shop on U.S. merchant sites via ShopRunner. Apple is aligning itself in China with the banks and networks who would like to blunt Alipay’s dominance in and outside of China. With a 14 percent share of phones and low NFC terminal penetration, combined with the very recent decision on the part of the regulators to relax the use of QR codes in stores to pay, Apple has a pretty big rock to push up that payments hill.

Of course, Apple also has tens and tens of billions in its bank account that could fund all sorts of incentives to get consumers and merchants over the hump. It may come to that. In order for Apple Pay to be more than just a domestic U.S. payments scheme, Apple will have to think differently about its ignition strategy.

But that’s precisely why the mobile payments game isn’t over by a long shot. On the global stage, it’s really just getting started.

{kind=link}