In June of 2014, Amazon launched the Fire phone. Priced at $650 and offered exclusively by AT&T, the phone’s big selling point was its “Dynamic Perspective” — a feature that provided a 3D experience using the phone’s camera, phone gyroscope and operating system.

And so was the fact that it was from Amazon, the world’s biggest online retailer.

Amazon’s thesis at the time: use its highly successful eCommerce platform as the cornerstone for a mobile ecosystem powered by the Fire OS, Amazon hardware and apps. With millions of consumers buying from Amazon every day, coupled with the consumer’s fascination with smartphones and apps — and about half the market for smartphones still up for grabs in the US in 2014 — what could go wrong?

In August of 2015, Amazon shut down the production of the Fire phone and stopped selling it soon thereafter. The company never said how many Fire phones were sold, which is probably indicative that it didn’t sell very many. I can’t name anyone who bought one — can you?

Getting consumers to ditch their Apple and Android devices and move to the Fire phone required more than the lure of a 3D experience and a promise that the apps consumers liked and wanted to use would be available, someday.

It was Amazon’s decision to use a forked version of Android that put a fork in their mobile ecosystem plans, so to speak. That decision created friction for developers, who had to adapt their app to a third operating system to reach Fire phone users. Developers had to be convinced there were going to be enough Fire phone users to make it financially worthwhile to spend the time.

There weren’t and so they didn’t, and you know the drill. No users meant no developers, no developers meant no apps, no apps meant no users. Network effects in reverse at rapid speed.

The failure of the Fire phone is a stunning example of platform strategy gone wrong by a company that could give a Masterclass in platforms, ignition, and network effects. But it’s also a reminder of the complexity of platform dynamics at work — and the outcome when the competition, and not the customer, becomes the center point of platform strategy.

| It’s a reminder of the complexity of platform dynamics at work — and the outcome when the competition, and not the customer, becomes the center point of platform strategy. |

Amazon wanted to compete with its Big Tech compadres — Apple and Google — both of which had phones and operating systems and app stores, and the lion’s share of the 55% of U.S. consumers with smartphones in 2014. Despite being a successful app on both Apple and Android devices, Amazon wanted an ecosystem of its own, and thought it needed its own mobile device to do that.

The company failed to consider that it would take more than the Amazon brand to persuade the millions of consumers who were already shopping with Amazon on other devices to make the switch.

We’ll never know what might have happened if Amazon decided against using a forked version of Android that fueled the death spiral that ended in the Fire phone’s demise. But we can see what happens when companies, even the biggest ones with the resources and know-how, fail to examine the sources of friction — and therefore the opportunities to create value — when designing and launching a platform from a cold start.

And that brings me to Paze.

You all know Paze, or maybe you need to be reminded — until last week, it had been a while since we heard from them. Paze, as I wrote earlier this year, was the worst-kept secret in payments when it finally went public with its plans to create a single mobile wallet that all bank customers could use to pay at the online point of sale.

Paze is the product of Early Warning, which operates the Zelle network. The seven U.S. banks who own it report having 150 million consumer debit and credit cards collectively. These seven banks are Bank of America, J.P. Morgan, Capitol One, PNC, Truist and Wells Fargo; many have ambitions, and projects underway, to create their own branded payments ecosystems.

At launch, the Paze CEO said that the wallet would be available for the 2023 holiday shopping season, which kicks off in early October with Amazon Prime Deal Days. He said that he expected Paze to be available as a checkout option on the top 200 eCommerce sites by then.

In a story published last week by The Financial Brand, we learned that rollout will be delayed until early 2024.

In that story, the Paze CEO was reported as saying more of a phased rollout is needed with more time to get merchants on board.

That’s the talking point.

Just like the Fire phone, the idea for Paze was cooked up as a way for banks to compete with the general-purpose Pays (Google and Apple) and PayPal. Its key selling proposition to merchants was that it would be free — but not really. The merchant is charged interchange based on whatever method of payment the consumer registers to her Paze wallet and uses to make the purchase. It is inconceivable that Paze and its seven banks would really make Paze free and/or give merchants a break on interchange to accept it. That would risk cannibalizing fee income from other online checkout options, including other wallets and buy buttons.

The “free” part is a shot across the bow at Apple, since banks hate paying the Apple toll when the Apple Wallet is used at the point of sale. Judging by the data, that hasn’t amounted to very much — at least not so far. The latest PYMNTS Intelligence data shows that PayPal is used 2.5 times more at online checkout than Apple Pay, with Apple Pay showing modest growth of 2.5 percentage points over the last three years to now 4.1% of online transactions.

From a merchant’s perspective, that seems to put Paze on par with every other checkout button, each of which has far more consumer adoption, usage and ubiquity than Paze.

| Without any sense that there will be consumer preference and volume to follow, incentives alone may not be enough for the top-tier merchants to play along. |

To accept Paze, merchants must take a leap of faith that consumers and incremental volume will follow — and they may require (costly) incentives to accept Paze in order to get the flywheel turning. Even then, merchants must divert resources to integrate it, support it and answer questions about it. Without any sense that there will be consumer preference and volume to follow, even incentives may not be enough for the top-tier merchants to play along — at least not now.

Just like the Fire phone in 2014, that puts the ball squarely in the consumer’s court.

Like the promise of Amazon shoppers and the Fire phone in 2014, having a collective consumer pool of 150 million debit and credit cards doesn’t mean that any — or enough — of them will make the switch. To do that, consumers must be convinced that the Paze experience is better, and then use it more than they use other alternatives today.

When Square launched in 2009, consumers toting those hundreds of millions of debit and credit cards were given an incentive to use them with taxi drivers and merchants, since the alternative was pulling out cash. That was friction for consumers and merchants, so using their plastic card credentials instead of cash was a no-brainer.

In 2023, the online competition is much stiffer.

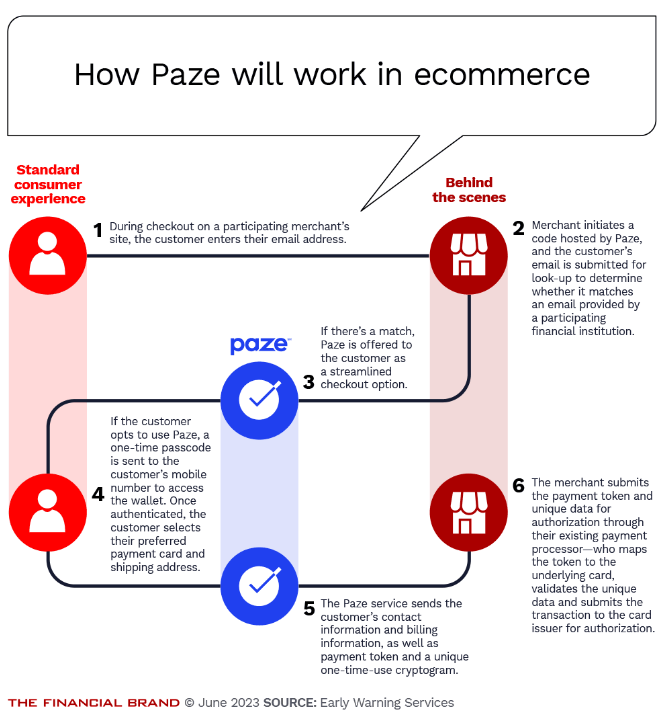

Paze touts a seamless checkout using the consumer’s email as the alias to a streamlined checkout. That alias is connected to registered card credentials prepopulated by the seven participating banks, and — according to a Paze blog — dynamically updated to offset the risk of a failed payment due to expired cards. And over time, randomly presented to the consumer based on Paze algorithms based on usage.

I have not personally seen a demo of Paze, but here is the flow according to the Financial Brand article, citing Early Warning documents.

A consumer enters her email. If the merchant accepts Paze, she will see an offer to pay using it. If she says yes, a mobile code is sent to her phone to authenticate herself, which then takes her back to the confirmation page to confirm shipping and payment credentials, and then to buy.

Lots of steps and lots of clicks.

This is happening while, according to brand new PYMNTS Intelligence data, 51% of consumers used biometrics instead of username and password to make their last purchase online. And 46% of consumers used stored (and tokenized) credentials in the browser (46%) or registered (and tokenized) cards on file (65%) to check out.

And as the digital world is moving to one-click checkout to eliminate steps, save consumers’ time and boost merchant conversion.

There are many checkout frictions to solve as time-constrained, digital-first consumers express growing degrees of dissatisfaction with the experiences that waste their time. One of the biggest opportunities we have in payments is to make checkout work harder for the consumer and the merchant without either having to work harder to benefit from that powerful, invisible smart payments experience. That’s why introducing extra steps in the process, pop ups that distract without any differentiating value, especially when consumers have other options available across all the sites they regularly shop, seems like a non-starter.

| Time-constrained, digital-first consumers express growing degrees of dissatisfaction with the experiences that waste their time. |

What consumers consistently say they want is an app that can aggregate their shopping, payments and transactional banking activities into a single digital experience. In fact, a PYMNTS study of 3,320 U.S. consumers finds that nearly 80% say this is what they would like to have and use. Not a super app, but an everyday app smart enough to curate and serve relevant prompts for things to buy or offers to consider — and secure enough to avoid the hopscotching around apps and webs and usernames and passwords to chase that information down.

We don’t quite know what form this will take or even how consumers envision the experience. Is it a digital front door? Is it an alias or tokenized payment and identity credential to unlock experiences across the online and offline worlds? We see many different players, with scale, pursuing these options and getting consumers on board — or improving the experience for the consumers that already use their payments product. That is where the exciting opportunity to innovate the checkout experience — on and offline — will emerge over the next several years.

That doesn’t seem to be where Paze is headed. And I suspect that the Paze we see now is a very different Paze than what was envisioned in the war room that gave birth to it a couple of years back.

I believe it was intended to be a payments network using consumer bank account credentials to pay merchants. And that it was met with a resounding thud by the same banks who have ix-nayed the use of RTP rails for the same reason. Not only is there a loss of fee income, but there is a reeducation of the consumer on the benefits of swapping her debit card or credit card that she knows how to use already for a bank account payment when making everyday purchases. Doing that requires answers to questions related to zero liability and refunds, chargebacks and disputes — all the things that are well-trodden in the card world, but absolutely a work in progress in the pay-by-bank-at-the-point-of-sale world. And the requirement for merchants and issuers to support an entirely new flow without a business model or evidence to support its adoption and usage.

I also believe that, as I stated in my original piece on Paze, the seven owner banks who said yes to the idea and put in a little money to see how it might work would ultimately be conflicted over how Paze operates in the wild. Banks compete for top of wallet, and a consumer-directed bank wallet operated by a bank consortium creates lots of weird dynamics for how that might work. What happens when a Bank of America checking account customer uses her Chase card to pay for most of her purchases on Amazon — which is standard operating procedure today? Would Paze algorithms prompt offers to move the Chase card to a BoA card? How would Chase feel about that? (Three guesses on the answer.)

And what is the business model for Paze? How do banks make money, and what’s in it for them if there is no incremental fee income from the rail itself? Is Paze a subsidy for another bank-centric scheme? If so, what? And how does any of this relate to what banks are doing on their own, and/or how the banks already on board the RTP network might use it for account-to-account payments?

There are also larger players, with scale, making inroads in the merchant pay-by-bank space with rails that connect consumers and third parties with this option. And other players that are making it easier for banks to use data to personalize options to use their products at checkout. All these options have scale, business models and momentum that create incentives to get consumers and merchants on board.

Those of us who’ve been in payments for a while have seen versions of this movie before — when the competition, not the customer, was the driving force for change. We saw MCX crash and burn, and other attempts to create merchant-centric networks sputter and fail to scale. We’ve seen network buy buttons disappear, and the effort to aggregate them into a single button — SRC — fade away, too.

| Those of us who’ve been in payments for a while have seen versions of this movie before. |

At the same time, we’ve seen the success of alternatives that add value to the checkout process — installment payment options offered in the checkout flow or BNPL options that give consumers with limited or no access to credit a way to burnish their credit profile and for merchants to snag a sale. Or the simplicity of registered credentials in browsers or on merchant sites, or branded buy buttons on the sites that consumers shop regularly that make checkout easy-breezy. For all of the merchant kerfuffle over interchange, cards drive conversion and sales.

An early 2024 launch makes it a year post-announcement for its real public unveiling. For Paze, like the Fire phone, getting merchants (or developers for Amazon) is critical. But solving a consumer’s problem is make-or-break. And building a solution around that is the opportunity. For Paze, that seems like a big lift — and a short period of time in which to deliver it.