Intense competition from online and mobile channels, pricing pressures and shrinking margins, high fixed costs, changing customer demographics, and eroding revenue opportunities.

Sound familiar? It should. It’s exactly what drove the newspaper industry into a death spiral about 20 years ago, and it’s what’s playing out right now and before our eyes in the world of physical retail.

Let’s turn the clock back 70 or so years. It’s the 1940s. There was one newspaper for every two adults. Newspapers and the companies that owned them were society’s information lynchpin and how people learned what was important. Then, 85 percent of adults got their news from newspapers.

Now let’s fast forward 20 years. The introduction of radio and TV has begun to slowly erode that grip, and now roughly 73 percent of adults get their news from newspapers. Twenty years after that, and only 55 percent do. The proliferation of television/cable TV and online/mobile outlets starting in the mid-to-late 1990s only made that slippery slope much, much, slicker. Today, less than 10 percent of adults say their primary source of news is the newspaper. Much of that decline took place in the last decade.

As you can imagine, the newspaper-revenue story is pretty grim. Paid circulation is down roughly 30 percent since the 1990s. Readers simply have more options, including many free ones, to get their news and information. And practically no one under the age of 30 reads a newspaper. (To be precise, according to Pew, only 6 percent of those ages 18 to 24 and 10 percent of those ages 25 to 30 say they do.)

|

Those who do, well, let’s just say they’re getting old. More than 50 percent of the physical newspaper audience is older than 65. Young people who don’t read the newspaper now aren’t growing up to take the place of those diehard readers headed in few decades to that great big reading room in the sky.

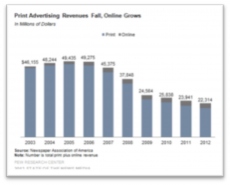

On the decline

Naturally, fewer eyeballs means that fewer advertisers want to pay for space. So print-advertising revenues are dropping like a stone, declining nearly 9 percent last year, even as overall advertising spend started to inch back up after years of suppressed spending following the financial crisis. Digital advertising, including mobile, hasn’t exactly saved the day either as expanding ad inventories has only driven ad prices down. The industry reports that for every $15 of print advertising lost, it gains only a dollar in digital advertising ― not exactly the kind of ratios that lets CFOs sleep well at night.

Other revenue opportunities have just disappeared altogether. Classified and recruitment/help-wanted and real-estate ads, which once were the domain of newspapers, are now dominated by such online outlets as job boards, portals like Realtor.com and Truila, and classified services like Craigslist. This upside down financial picture means it’s increasingly harder for newspapers to pay the bills, including recruiting good journalists to write great stuff that could attract more eyeballs. And, without eyeballs, there’s no compelling story to sell to advertisers or other third parties, whose revenues would subsidize getting the better content that would attract more eyeballs. And without a good content/revenue model, investors look the other way too.

You get the point. Death. Spiral. Ok, it’s not a quick death like being

|

hit by a bus, and maybe there will always be a little bit of life allowing newspapers to survive in a limited way. But for all intents and purposes, the newspaper of the olden days has seen the Grim Reaper and knows its days are numbered.

Although TV and radio slowly chipped away at paid circulation and advertising through the 1980’s, newspapers’ rapid descent into a death spiral was brought about by the proliferation of online and mobile alternatives, which introduced new access channels and new content that attracted the interest of its existing and prospective customer bases. And once the fewer readers/fewer advertisers circular loop got momentum, it became mighty hard to stop and downright impossible for many to live to tell the story of how they survived it.

So today, the newspaper industry is about half the size that it was in the 1940s. The survivors are the mega big guys, such as the Wall Street Journal, the Financial Times, the New York Times and USA Today. They have vast “omnichannel” outlets and scale from which to extract revenues and allocate costs ― paid subscriptions, advertising, conferences, reports, data, multimedia/digital platforms ― and great content and content contributors for which people and advertisers are willing to pay for access. But some of them, like the New York Times, even struggle to post profits and have seen recent softening in national advertising sales. Most continue to experiment with ways to expand revenue beyond traditional advertising and subscription models.

Regional players like the Boston Globe, the Washington Post, LA Times, etc. are getting creamed ― so much so that billionaires such as John Henry (Boston Red Sox) and Jeff Bezos (Amazon) can add once-storied franchises like the Boston Globe and The Washington Post to their billionaire trophy shelves for not much more than they’d pay for some artwork to hang on their walls or a small island.

You need look no further than your own hometown newspaper for evidence of this. I was visiting my parents last week in Baltimore, and they have been getting the Baltimore Sun delivered every day for more than 50 years. This used to be one of the great American newspapers and was home to the very famous essayist H.L. Mencken. Man, has it become a pretty pathetic paper. The front section is about six pages of regurgitated AP press releases, mediocre local political stories and obituaries, which are, I swear, the only reason my parents still get it delivered. At their ages (79), they are obsessed with seeing who has died. But even my parents now go online to get their news from a variety of sources, which is now made even easier with their iPads in hand.

The survivors also include, quite ironically, the community papers. Warren Buffet isn’t called the Oracle of Omaha for nothing – he’s been investing in them like crazy. They seem to fill a gap that serves up important community information, including local news, the essential social scoop/gossip and local advertising. These papers are typically published once a week, operate with lean staffs, carry lots of local advertising that’s pretty competitively priced and carry much lower expectations of the quality of its content so the fixed costs are low. After all, no one is expecting Pulitzer Prize winning journalists to write stories about the new store that’s opening on Main Street or changes to the local zoning laws.

Let’s get physical – retail.

It’s the 1950’s, and the birth of the shopping mall. Before then, all shopping was done at local merchants. Malls changed all of that, making the shopping experience efficient (lots of stores under one roof), social (it was something women and friends and families did together) and fun (there was lots to do). All shopping was done in physical stores and, increasingly, away from the local merchant scene that had defined retail for centuries.

In 1999, five years after the launch of Amazon.com and the year in which Jeff Bezos was named Time magazine’s Person of the Year, eCommerce accounted for only 0.5 percent of retail sales. Even today, with the diffusion of the Internet and mobile devices, eCommerce accounts for less than 6 percent of all sales, but it’s growing rapidly.

In those “good old days,” retailers focused mostly on competition from the merchant across the street or worried that a certain merchant with headquarters in a certain southern state that begins with the letter “A” would move into their turf. Then two things happened: the Great Recession of 2007, and the birth of the daily deal in 2008.

Financially strapped and budget-conscious consumers followed the deal, regardless of any brand or store loyalty they once may have had. The “new normal” for consumers was 50 percent off, and it didn’t really matter who offered the deal. Retailers, in an effort to bring consumers back and keep them loyal, responded by decreasing inventory levels on the theory that scarity of supply would drive spend at non-discounted prices.

They also implemented “loyalty” programs that cost them a bundle to acquire customers. The results are pretty ugly. When adjusted for inflation and population growth, retail sales today remain well below pre-2007 recession levels and show less than a 25 percent increase overall over the last 20 years. Profits have taken a big hit.

Another thing also happened on the way to this new physical retail environment: the rapid adoption and utility of the smartphone. Consumers, armed with these smart mobile devices literally 24/7, used them to shop online. In 2013, more than half of all eCommerce sales originated from mobile phones or tablets. Not only do mobile devices make it possible for consumers to shop anytime and anywhere, it gives consumers access to pricing and product information anytime and anywhere. That sets them up with a powerful new tool that helps them get the best price for the products they want to buy.

Show me the showroom

Smartphones have also turned retail storefronts into showrooms. Starting in the holiday season of 2010, consumers began using their mobile phones to check out prices and reviews and recommendations on items of interest while standing in front of them, only to buy those products online roughly a third of time, according to analysts. But as much as showroomed retailers hated the notion of sales literally walking out the door, they took solace in the fact that they still drove 96 percent of retail sales, and online sales were a very small fraction of their overall sales. Physical retailers had a steady, sizeable and captive audience walking through their storefronts that they could sell to and monetize.

Or so they thought.

|

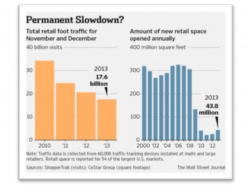

What has sort of hit everyone in the face like the sub-zero wind chills from the 2013/14 Polar Vortex is something that has retailers shivering just as badly: the documentation of a steady but dramatic decline in foot traffic in their stores over the last three years.

The Wall Street Journal reported last week that during the 2013 holiday shopping season, retailers experienced 50 percent less foot traffic in their stores than they did three years earlier. As in 5-0 percent. The declines were quite dramatic too: 28.2 percent in 2011, 16.3 percent in 2012, and nearly 15 percent in 2013.

At the same time, online sales were up more than 50 percent, with much of that attributed to commerce enabled by smartphones and tablets. People this past holiday season, at least, literally voted with their feet, and they decided they didn’t want to use them to trapse through malls and stores to buy what they needed.

A few things then started to click for me. One of my Facebook friends posted how wonderful it was to shop at a very chi-chi mall in Northern Virginia the Saturday before Christmas because it was so empty. She and her husband made a day and evening of it and plan to make it an annual occurrence. Well, that’s assuming that the mall and the stores they like to shop in the mall stick around.

I had the same experience that same Saturday but in downtown Boston. I was rushing around doing a bunch of last-minute shopping and expected to be duking it out with the other last-minute shoppers. To my surprise, I found a parking spot easily, didn’t have to navigate my way around throngs of shoppers, and found super-helpful salespeople to assist me, including one who volunteered to help me carry my packages to the car. Even Boston’s famous Newbury Street, which is typically jammed packed with shoppers on any given Saturday, seemed leisurely.

The online movement

After reading this WSJ article, I decided to ask people ―all sorts of people ― about their shopping habits this holiday season. What I heard was remarkably and surprisingly consistent. Most, if not all, did “most” of their shopping online, not to the exclusion of going to the store, but the ratio of online to offline was something like 80/20, including my 79-year-old parents.

When I asked why, here’s what I heard:

One reason was related to the calendar itself: there were just fewer shopping days before Christmas this year, and there wasn’t enough time for already-busy people to go to the store and prepare for the holiday. Online just made shopping easier, especially because so many stores offered free shippping up until the very last minute, and just about anything that anyone wanted to buy was available online.

But the second thing that people said about their shopping habits this holiday season was really, really, interesting. When people did go to a store, they went there on a mission. Even the women. They had done their research online, knew what they wanted to buy, and then just went in and, wham bam, got what they went in to buy and left. It wasn’t as if people didn’t go to physical stores to buy stuff, they just made fewer trips to fewer stores, spent less time while there and walked out with fewer things.

Turns out, my random little survey is borne out by national stats. In 2007, each time someone went “to the store” they visited 5 of them. Today, they visit 3. And, they’re purposeful ― going in to buy what they have researched online, and nothing more.

And, that’s really bad for physical retailers. What physical retailers want most of all is people in their stores, milling around and being tempted by the stuff that isn’t on sale or stuff that falls into the “impulse” category. Sure, they advertise a sale on cashmere sweaters to draw in customers, but what they really want is for that customer to buy that sweater (or maybe another one that they like better that isn’t on sale), plus the skirt, jacket and shoes that go with it. But that’s not what people are doing. They’re going in to buy the sweater on sale and then vamoosing. Lingering concerns over the economy and chronic un and under-employment have consumers more cautious than ever about opening their wallets and shopping like it was 1999, or 2006, as the case may be.

And that’s sort of a bummer. If you are a store in a mall, it’s even worse since malls aren’t exactly the healthiest of retail artifacts these days to begin with. We haven’t seen a new shopping mall open in the U.S. since 2006, and vacancy rates at the ones that exist are at their highest levels since 1991, according to industry analysts. Anchor stores in a mall, like a Macy’s or JCP, bear pretty high fixed costs. And long-term leases were negotiated when online was an infant and mobile was an embryo. For these stores, keeping the lights on depends on lots of foot traffic and impuluse buys, and those were the financial assumptions made when setting up shop there.

The smaller stores that line the perimeter of those malls are there for one and only one reason: to benefit from the foot traffic from shoppers on their way to those anchor stores. But if time-crunched and budget-conscious shoppers are in and out of the mall, on their own missions and visiting fewer stores while shopping online in between, that’s not happening.

The Ghost Mall

So the little guys are forced either to move out or die. And then the no stores => no shoppers => no interest from new merchants to set up shop => no shoppers => no sales => no merchants => empty mall dynamic is set in motion. The end result for the mall, though, is the same ― vacant storefronts, which don’t exactly send such a warm and fuzzy signal to shoppers. It becomes sort of like the empty restaurant syndrome: no one wants to take a chance on eating in an empty restaurant,even if it advertises the best chef and a great menu. And no one wants to shop in a ghost mall.

So that faint whooshing sound you’re hearing? Yep, that’s the sound of the physical retail death spiral revving up. (Now this isn’t exactly like the newspaper death spiral. and I’ll tell you why in a minute ― just hang in there!) And the proof is in the sales numbers pudding. Absolute dollar sales for the 2013 holiday season may have been up slightly, but heavy discounting designed to lure shoppers in kept overall profits very soft.

Here’s another interesting anecdote. I was picking up a gift card at Neiman Marcus that same Saturday before Christmas and walked through the handbag department on my way to getting that done. I noticed that one brand that had a huge presence there ― Prada ― was gone, and another decent, but not as popular, brand was in its place. When I asked about that, I was told that Prada and Gucci were both pulling all of their merchandise out of Neiman’s and selling only in their own licensed stores and online ― clothing, handbags, shoes.

That’s a pretty important development. Brands like Prada and Gucci actually pulled in shoppers to Neiman’s and other department stores. These designer brands needed high-end physical retailers to sell their merchandise since they didn’t have online sites designed for commerce, and their company stores were scarce and not convenient for most people to access.

Today, these brands have commerce sites, and they are opening storefronts in many more cities. In fact, Prada opened 75 stores in 2011, 80 in 2012 and 2013, and it is planning to open 100 more stores in 2014 and 2015, going from 388 stores in 2010 to more than 670 in 2015.

This changes the physical retail sales dynamic for department stores in a material way. Brands like Prada now don’t need to rely on them to hawk their products. They can now go direct to their existing and prospective customers either online or through their own storefronts, preserve their margins, control the experience, offer consumers a bigger selection, and develop a direct relationship with that consumer across both the on and offline channels. And consumers have less of a reason to visit the department store.

Big gaping hole

Where does all of this leave physical retail in the years to come? Depending on who you are, possibily in a world of hurt. If you’re a department store, maybe you didn’t notice but the Grim Reaper has already paid you a visit. Shoppers are deserting you, and brands will too, leading to more shoppers deserting you and so on. That leaves a big gaping hole that doesn’t help pay the fixed-cost bills. If you’re a small store at a mall, you’re a passenger on a sinking ship. And if you own a shopping mall, well, better start making plans to turn them into lifestyle centers or rent them out for wedding receptions or Sunday church services. (Don’t laugh, some malls are actually doing this).

But unlike newspapers, physical retail as a category isn’t going to die. Physical newspapers are like the typewriter, products that people don’t want because they don’t need them anymore. New and better and more timely information products and delivery channels have taken their place. Big newspapers that could pivot to become efficient information and content providers with new different business models will survive, as will the local providers with completely a different cost structure and content focus. The vast undifferentiated middle will live on only in the history books.

But unlike newspapers, people still want and need physical stores. Most people, when asked, like to see and feel and touch things before they buy them. They want specialty stores and value the services that they get from them. Just walk by any Apple Store or a J.Crew store on any given day. Even though both brands make it easy to buy online, , consumers still like the physical-store experience. They like the atmosphere, the “vibe,” the people and the service. They like seeing and playing with new merchandise and get value from interacting with helpful sales associates. Absent that product/service mix and the experience that it creates for consumers, just like the physical newspaper, other online outlets would simply trump the interest in visiting a physical store.

The implication is that to survive, physical retailers must offer an experience that can’t be found or replicated online, one that will most obviously be different for different categories of retailers. That’s where some of the local mom and pops may have an edge and why they are embracing mobile apps with loyalty wrapped around payment and integrated POS systems with a vengenance. It’s also why mobile payments and commerce is igniting in food services; consumers may be able to use apps to order online and move to the front of the line to pick up their order in store, but food service,any way you cut it, is still a physical retail experience.

To survive, physical retailers must also embrace the Internet and the new connected device reality, and do it in a hurry. Omnichannel, as a strategy, must go well beyond using a word to describe having a presence in the online and offline worlds. Omnichannel must deliver a shopping experience that allows consumers to interact with merchants regardless of where and when they want to make a purchase and to receive the same level of service and merchandising across these channels. Omnichannel must also counter what’s becoming a key driver in purchasing decisions and makes it easier than ever to buy something online without seeing it first – customer reviews and ratings. Thanks to customer reviews and ratings, even products like cars that consumers only bought in a physical retail environment can be purchased, with confidence, sight unseen online.

Looking ahead, that means most of the big physical retailers we know and love today are probably hosed. The big ones, like that certain retailer whose name begins with a “W,” can operate at scale and make it efficient for people to make one trip and buy lots of the stuff that they need, including groceries, and offer lots of complementary services that they want, including financial services. They are like the New York Times and the Wall Street Journal ― known brands with scale and a variety of products and services to offer.

But most physical retailers likely will find it way too hard to reinvent themselves in light of their high fixed costs and to adjust their business models in a way that makes money at the same time they deliver value to consumers. Sure, they could start using their storefronts and inventory-management systems to fulfill orders from online customers and even collaborate with online marketplaces to accommodate same-day delivery, and some even are. And that strategy could work well for certain retail categories and offer a lifeline for some retailers for some period of time. But the convenience of online commerce and the reliance by consumers on mobile/connected devices, which makes shopping online easier and more efficient, has bred a whole new class of connected consumer who moves between shopping “worlds” with ease and with access to “perfect” information about product availability, price and consumer reviews. And that, when combined with the legacy infrastructure of existing physical retail, will force the development of a new kind of physical retailer.

So, my take? Many physical retailers, not physical retail overall, are headed for a death spiral.. Reinvention of the physical retail sector is essential, and like Darwin’s theory, only the fittest will survive. Over the next couple of decades, many of the large retailers we know and love today will either shrink or die, and a new breed of physical retailer will emerge to take their place. Survival will require retailers to focus their time, energy and investments on the things that matter most – making consumers want to buy from them. At the end of the day, nothing else really matters.