Rampant data breaches have left consumers on edge about digital fraud. They are not only anxious that their personally identifiable information may be compromised, but also skeptical that their financial institutions (FIs) would be able to spot fraud when it happens.

Rampant data breaches have left consumers on edge about digital fraud. They are not only anxious that their personally identifiable information may be compromised, but also skeptical that their financial institutions (FIs) would be able to spot fraud when it happens.

In fact, recent PYMNTS research shows that most consumers believe they can do a better job of identifying and protecting themselves against fraud than their FIs, with 71.2 percent saying they believe the security of transactions being made via mobile banking apps would be stronger if they had greater control over those apps’ authentication requirements. Similarly, 54.1 percent believe the chances for fraudulent transactions would decrease if they had more control over those requirements.

In fact, recent PYMNTS research shows that most consumers believe they can do a better job of identifying and protecting themselves against fraud than their FIs, with 71.2 percent saying they believe the security of transactions being made via mobile banking apps would be stronger if they had greater control over those apps’ authentication requirements. Similarly, 54.1 percent believe the chances for fraudulent transactions would decrease if they had more control over those requirements.

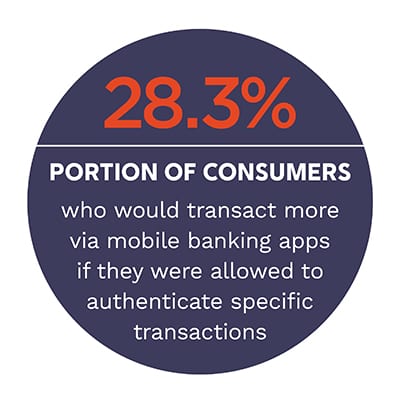

Despite widespread demand for greater mobile banking authentication controls, only 39.9 percent of consumers say their mobile banking solutions allow them to implement transaction-specific authentication requirements, and only 34.3 percent are given the option to choose the type of authentication methods they want to protect their mobile banking app transactions’ security.

How can banks help provide their customers the peace of mind they need to feel confident that their mobile banking authentication systems are strong enough to protect them from fraud?

This is just one of the many questions PYMNTS set out to answer in the Consumer-Centric Authentication Study: Transforming The Consumer’s Digital Banking Experience, in collaboration with Entersekt. We collected and analyzed survey response data from 2,835 American consumers to learn how and wh y they believe having greater authentication controls can enhance the security of transactions made via mobile banking apps, what banks can do to meet their customers’ demand for greater authentication controls and the barriers that need to be overcome to increase mobile banking app adoption.

y they believe having greater authentication controls can enhance the security of transactions made via mobile banking apps, what banks can do to meet their customers’ demand for greater authentication controls and the barriers that need to be overcome to increase mobile banking app adoption.

Our research shows that it is not enough for banks to simply authenticate users when they log into their accounts — the majority of consumers want their banks to authenticate just about every type of mobile banking transaction there is. Whether sending money to friends and relatives (65.5 percent of consumers cite this use case), paying merchants and contractors (64.5 percent) or using mobile card controls (63.5 percent), the majority of consumers say they want those transactions to have authentication requirements.

There are many reasons for this. According to our survey, 66.6 percent of consumers say having more authentication controls would make them feel safer and 38.3 percent say the added security is worth the extra time it takes to authenticate transactions. Many consumers also believe having more control over auth entication would improve their ease of use, for example, with 43.1 percent saying so.

entication would improve their ease of use, for example, with 43.1 percent saying so.

Many consumers say they want more than just increased control over authentication requirements, though. They also want more control over how their digital banking transactions are authenticated. Twenty-five percent of consumers say they want more than one option regarding how to authenticate merchant and contractor payments, and 25 percent want more options for authenticating the transfer of funds to friends and relatives.

Yet, examining consumers’ demand for more authentication controls is only the first part of a broader discussion of consumers’ complex relationships with their mobile banking solutions, their FIs and the digital banking transactions they make.

To learn more about what consumers want from their mobile banking authentication requirements and what FIs can do to help meet those demands, download the report.