You can see it in the quarterly earnings reports this year of just about every publicly traded company and among the list of companies that have either gone public one way or the other or have filed S-1s because they plan to do so soon.

You can see it in how investors are putting money to work in both consumer-facing and B2B startups, and how startups and incumbents are forging new partnerships to move innovation faster to market.

And you can see it in the hustle by retailers and brands large and small to pivot their businesses and business models — and the disclaimers on just about every retail site starting a week or more ago that orders placed online might not make it in time for Christmas.

It’s the impact of the digital-first consumer on nearly every one of the 10 pillars that define our connected economy — and the efforts of companies large and small to capture their attention and their business.

This is a consumer who, after nine long months of living in a world reshaped by COVID-19, has grown accustomed to the digital-first way of life — and likes it. The shifts that were forced when the world locked down and people realized it was safer to stick close to home, have gone mainstream out of the sheer convenience and efficiency of living in a digital-first world.

Over the last nine months, consumers have shifted to digital methods of working; shopping; banking; having fun; staying connected with family, friends and colleagues; paying and being paid; and acquiring three of the most basic of human needs — food, clothing and even shelter — as the buying and renting of homes and apartments has become digital-first, too.

Source: PYMNTS.com longitudinal study of over 40,000 consumers (data from the most recent panel on Nov. 11)

Source: PYMNTS.com longitudinal study of over 40,000 consumers (data from the most recent panel on Nov. 11)

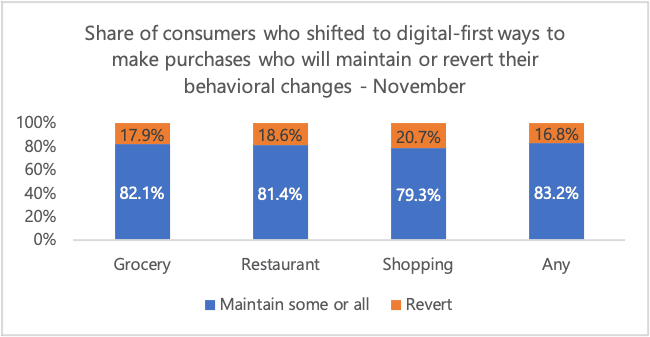

One hundred and ten (110) million U.S. consumers — 47.2 percent of the U.S. adult population — have shifted digital since March to shop for retail products, buy and eat food from restaurants, and buy food at grocery stores. This digital shift — doing less in the physical world and more in the digital world for the same activity — is based on 16 longitudinal studies that PYMNTS has conducted of a national sample of more than 40,000 U.S. consumers since March.[1]

Source: PYMNTS.com longitudinal study of over 40,000 consumers since March (data from the most recent panel on Nov. 11)

Source: PYMNTS.com longitudinal study of over 40,000 consumers since March (data from the most recent panel on Nov. 11)

Think about that for a minute.

In the space of nine months, nearly half of the U.S. adult population has made digital-first a way of life in some way. Almost half, 45 percent, have shifted digital to shop for retail products, and one in five to shop for groceries and order food from restaurants.

Even more compelling is that 83 percent of these digital shifters say they will stick with some or all of those digital-first habits — even when they are able to interact in the physical world without the fear of COVID, even though the majority of Americans don’t think that will happen before January of 2022.

The PYMNTS data supporting the permanence of this shift has remained largely consistent for every one of the 16 studies we have done and across geographies and demographic groups. Just as many boomers have made the digital shift as millennials, and as many of those living in big cities and towns have made the shift as those living in less populated areas.

This “and-we’re-not-turning-back” digital shift is the topic of conversation for many — and for many reasons — including the now bipartisan “Big Tech is Bad Tech” conversations taking place on Capitol Hill and throughout the media.

Those conversations have largely ignored the Biggest Tech company of all, Apple, and Apple Pay. Although the wagons have begun to circle more publicly and more recently on Apple and its payments stance — given the very public lawsuit over in-app purchases — large-scale efforts to challenge Apple’s position on allowing anyone other than Apple access to the NFC chip haven’t gotten much media bandwidth.

That may not be the case for long.

There are two physical points of sale that could become ground zero for contactless on Apple devices: the traditional terminals sitting on the counters at retailers all over the world, and the iPhones and tablets that, helped by Apple’s acquisition of Mobeewave last June, have turned into POS terminals for anyone who wants to accept contactless payments.

Apple Pay’s Digital-First Disconnect

Apple has long said that it ixnays anyone but Apple, and anything but Apple Pay, from accessing the NFC chip needed to make a contactless purchase at a terminal in a store because of security concerns.

Critics scoff and say the company has stifled innovation by preventing access to the iPhones in the hands of almost a billion consumers around the world, who transact and spend more when they shop in a physical store.

Source: PYMNTS.com survey of 2,683 consumers conducted between Nov. 23-25, 2020

Source: PYMNTS.com survey of 2,683 consumers conducted between Nov. 23-25, 2020

Granted, it’s always hard to prove a negative, but not having access to the NFC chip has likely prevented innovators from investing time and money in developing the innovations that could have made the in-store POS experience better for iPhone users. And since iPhone users skew more to the affluent, it also denied those innovators the opportunity to monetize their spend.

Critics also claim that it’s hurt consumers. And it probably has.

Consumers are accustomed to using apps on any connected device because developers create apps that cross platforms and ecosystems. Many of those are payment apps used by consumers online, but not in brick-and-mortar stores without access to Apple’s NFC chip.

Take PayPal, for example. According to a national study conducted by PYMNTS of 2,683 consumers on Nov. 5, nearly four times more consumers prefer using PayPal to Apple Pay online, but no PayPal user with an iPhone can use her PayPal wallet as a contactless payment method at the physical point of sale.

Apple Pay’s position on denying access to its NFC chip might also not been a great idea for Apple, unless it has something else up its sleeve.

On the sixth anniversary of the launch of Apple Pay in November, a PYMNTS study of some 7,585 U.S. consumers showed that of the 7.75 percent of eligible sales in a physical store (a person with an iPhone making a purchase in a store that accepts Apple Pay), only 2.65 percent of purchases in stores that accept Apple Pay were made using Apple Pay, representing just about 1.53 percent of all retail sales.

[Table 1: Share of U.S. adults with eligible devices and sales from retailers that accept Apple Pay]

| 2015 | 2017 | 2019 | 2020Q1 | 2020 | |

| Share of U.S. adults that have an eligible device |

|

||||

| % of adults that use smartphones | 69.0% | 77.1% | 81.0% | 81.9% | 82.4% |

| Share of smartphones with correct OS | 42.7% | 43.5% | 47.0% | 47.4% | 47.1% |

| Share of iPhones that work with Apple Pay (6 or newer) | 39.2% | 87.0% | 89.8% | 92.8% | 93.9% |

| Share of individuals that have an eligible device | 11.6% | 29.2% | 34.2% | 36.0% | 36.4% |

| Total estimated eligible sales (in billions) | |||||

| Total retail sales (excluding automobiles and eCommerce) (in billions) | 3,934 | 4,147 | 4,432 | 4,212 | 4,212 |

| Share of merchants where the wallet is accepted | 19.4% | 23.4% | 51.1% | 54.3% | 57.6% |

| Total sales from merchants that accept the wallet (in billions) | $762.7 | $968.8 | $2,265.9 | $2,285.1 | $2,425.2 |

| Total estimated sales at eligible merchants to U.S. adults that have the correct device (in billions) | |||||

| Potential value of sales using the wallet (in billions) | $88.1 | $282.7 | $775.0 | $822.9 | $884.0 |

| Usage Summary | 2015 | 2017 | 2019 | 2020 Q1 | 2020* |

| (1) Percentage of eligible transactions that used the wallet | 5.10% | 6.90% | 6.05% | 4.9% | 7.75% |

| (2) Percentage of eligible stores’ shoppers that used the wallet | 0.59% | 2.01% | 2.07% | 1.64% | 2.65% |

| (3) Estimated percentage of in-store sales where the wallet is used | 0.11% | 0.47% | 1.06% | 0.89% | 1.53% |

| Estimated sales where the wallet is used (in billions) | $4.49 | $19.51 | $46.85 | $64.34 |

Source: PYMNTS.com survey of 7,585 consumers conducted in October 2020

Source: PYMNTS.com survey of 2,683 consumers conducted between Nov. 23-25, 2020

Source: PYMNTS.com survey of 2,683 consumers conducted between Nov. 23-25, 2020

In fact, good-old cash at the physical point of sale is preferred by consumers nearly three times more than Apple Pay. That’s according to PYMNTS’ study of a national study of 2,683 consumers conducted on Nov. 5.

And when PYMNTS asked 3,887 consumers on Nov. 11 2020 how they paid for their last purchase in a 24-hour period, only 1 percent said they used Apple Pay.

Could those numbers have been different if more innovators had more access to Apple’s NFC chip and used Apple Pay’s contactless infrastructure to create a flywheel for contactless mobile payments in-store?

Maybe, even though the performance of any of the “Pays” at the physical point of sale has been pretty lackluster — including Walmart Pay, with its captive audience of Walmart customers and ubiquitous acceptance.

And therein lies the rub.

The “Pays” — and Apple Pay as the granddaddy of all of the mobile contactless wallets — didn’t solve a problem at the physical point of sale when it launched in 2014, since cards worked just fine.

And the Pays still haven’t.

Source: PYMNTS.com survey of 2,185 consumers conducted on Aug. 25-31, 2020

Source: PYMNTS.com survey of 2,185 consumers conducted on Aug. 25-31, 2020

It’s true that contactless at the in-store POS has been elevated to an essential service for consumers who shop there. According to a recent PYMNTS study, 60 percent of consumers say that enabling contactless and touchless experiences at the point of sale is an important factor in deciding which merchant gets their business — but not necessarily contactless digital wallets. Contactless cards are regarded as decision-drivers for shopping in a physical store 7.5 percent more than using a contactless mobile wallet.

It’s clear from the data, at least in the U.S., that Apple Pay hasn’t seen much of the COVID tailwind that has propelled the adoption, use and growth of the many digital apps players — which do more than just offer consumers a different way to pay in a store.

Further, some recent reports about Apple Pay and contactless at the point of sale are flat-out inconsistent with repeated surveys of American consumers. One even claimed that Apple Pay is the third-most-popular mobile wallet behind Alipay and WeChat Pay. I suppose it all depends on whether the definition of “popular” also means most-used. If this was remotely close to being true, Apple would be shouting those financials from the rooftops.

The Digital-First Consumer

The weekend after Thanksgiving and the two weekends before Christmas are typically when I shop local. It can be both fun and festive. I often visit the same shops year after year, so I know the shopkeepers and they know me, which adds an important personal touch to those shopping excursions.

COVID made shopping at those stores much different this year.

Instead of visiting the shops in person, I did what some of you probably did: I shopped online and picked up my items curbside.

This year, one encounter with one small, local merchant stood out.

As I browsed her site and filled my shopping cart, I had a few questions about several items. I punched out to the live chat feature and asked my questions. Within a minute, I was chatting with the owner, who also suggested that I reconsider one of the things in my cart — she didn’t think I’d like it and suggested something else instead. I took her advice, asked when I could swing by and pick up my goodies and completed my purchase online. She thanked me profusely for shopping small. I was happy to support her business.

The whole process took less than 15 minutes.

Don’t get me wrong — I did miss being out and about (especially over this past weekend, since there is a lot of still very white snow here in Boston, which makes everything seem even more festive). And I pray that next year’s shopping experience will be filled with that holiday hustle and bustle.

But the ability of this small Main Street shop to use modern POS technology to offer me (she uses Shopify) and her other customers a slick and efficient digital-first shopping experience meant that she got the business, and I could shop in the way that was most comfortable for me this holiday season.

She didn’t care how I paid for what I bought, or whether I was standing in front of her POS terminal in the store when I did it. The most important thing was that I bought — and that she didn’t lose a sale to someone who didn’t want to shop and pay in her store and didn’t have any other way to buy.

What’s Next

To shop or not to shop — and to pay or not to pay — in the physical store is the trillion-dollar question being posed as the behaviors of 2020’s 110 million digital shifters are becoming more clear, and as merchants of all sizes and types are pivoting to meet the consumer where and how she wants to shop.

Paying, of course, has always happened at the end of the shopping journey at checkout — but in a digital-first world, where the buying happens online, checking out means hitting “buy.”

The physical store serves a different purpose, forcing a rethink of the customer’s shopping journey in a digital-first world — one in which digital has become an integrated part of the physical store experience.

Yet over the last six years — and even as recently as Apple’s latest earnings report — Apple Pay continues to focus on the “pay” part of the commerce experience. And contactless payments is where Apple CEO Tim Cook says he sees tremendous potential.

Unfortunately, that’s not where the digital-first puck is heading — but that doesn’t mean Apple isn’t in the mix. One of the most successful mobile payments apps, offered by Starbucks, is an iPhone app — and people can use their iPhones in China to pay with their Alipay and WeChat Pay apps. Of course, these are on Android phones, too.

Maybe if Apple opened up the NFC chip to others, it would support more apps for physical payments — even ones that consumers could use with the billion iPhones that Apple would like to turn into contactless mobile terminals.

But, really, the digital-first puck is heading to using smartphones, like the iPhone, and other connected devices to pay in a way that doesn’t involve a consumer interacting with the so-yesterday terminal at the physical point of sale or even being inside brick-and-mortar shop. Innovations that give consumers touchless payments options — card on file, QR codes — and digital wallets, and the “super apps” that cross channels, platforms and operating systems, giving them more than just a way to pay.

A future where the consumer is the point of sale and her connected devices, her personal and personalized remote control for deciding how and where to buy — where payments are invisible and just come along for the ride.

[1] These data are from the longitudinal studies from March 6 through Nov. 11.