Access to financial services is a constant struggle for millions of Americans, with more than 6 percent of American households remaining unbanked and nearly 19 percent considered underbanked. Households with lower incomes are especially likely to lack access to bank accounts, with 19 percent of families earning less than $30,000 in annual income reportedly unbanked, compared to just over 2 percent of those with higher incomes.

Access to financial services is a constant struggle for millions of Americans, with more than 6 percent of American households remaining unbanked and nearly 19 percent considered underbanked. Households with lower incomes are especially likely to lack access to bank accounts, with 19 percent of families earning less than $30,000 in annual income reportedly unbanked, compared to just over 2 percent of those with higher incomes.

Offering debit solutions, such as prepaid cards, is a key approach that can help financial institutions (FIs) appeal to unbanked and underbanked consumers. These low-fee cards avoid the issues that drive many customers away from traditional credit, like excessive fees or overdraft charges. Analyzing next-gen debit solutions and how they can benefit unbanked and underbanked consumers should be top of mind for both banks and merchants moving forward.

In the July Next-Gen Debit Tracker®, PYMNTS explores the latest in the world of debit, including the plight of unbanked and underbanked individuals around the country, the challenges they face as a result of their lack of access, and how next-gen debit solutions can help aid in these struggles.

Developments From The Next-Gen Debit World

Some of the underbanked populations in the country are also the most vulnerable including immigrants, 13 percent of which are part of unbanked households and 26 percent are considered underbanked. Remittance provider Remitly is among those utilizing debit as a potential solution, adding new features to its mobile app, Passbook, to expand immigrants’ access to low-fee debit options. The features include new peer-to-peer payment features as well as early payday services. It will also enable users to access virtual debit cards while they are waiting for physical cards to arrive in the mail. The offering allows consumers to purchase goods with ease while also reducing their reliance on payday loans and other predatory lending services.

Some states around the U.S. are also exploring options to improve financial access to the underbanked. California Assemblyman Miguel Santiago (D) recently introduced the California Public Banking Option Act, a regulation that would grant state residents access to a no-fee debit card from BankCal, a state-run “public bank.” The goal of the program is to open up access to financial services for unbanked or lower-income individuals, as those making less than $15 per hour make up the majority of unbanked consumers within the state. The proposal has drawn limited support from Californian banks, credit unions and other FIs, in part because the BankCal program will be state-supported. The act is now under review by California’s Appropriations Committee.

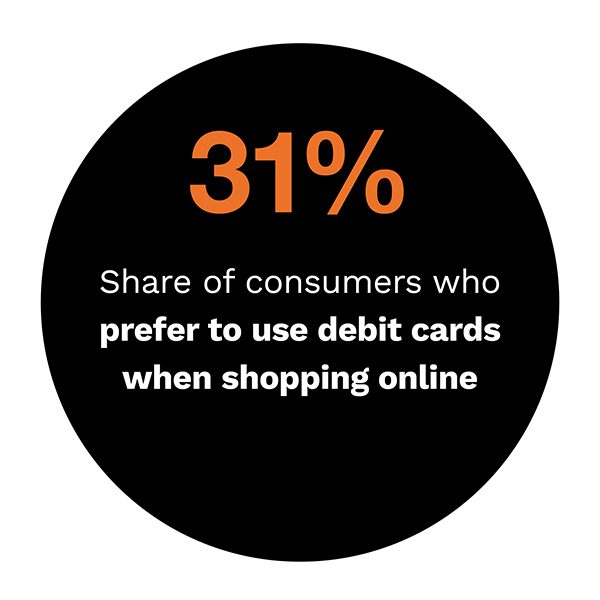

FIs and  merchants could also stand to greatly benefit from improved banking access. Recent research found that bank debit — also known as automated clearing house (ACH) debit — is the most widely used payment type in Australia, France, Germany, New Zealand and the United Kingdom. Consumers in North America preferred debit cards, with millennials and members of Generation Z being the most likely users. The research also discovered that consumers are nearly twice as likely to have access to debit cards, bank-to-bank payments or bank accounts than paper checks.

merchants could also stand to greatly benefit from improved banking access. Recent research found that bank debit — also known as automated clearing house (ACH) debit — is the most widely used payment type in Australia, France, Germany, New Zealand and the United Kingdom. Consumers in North America preferred debit cards, with millennials and members of Generation Z being the most likely users. The research also discovered that consumers are nearly twice as likely to have access to debit cards, bank-to-bank payments or bank accounts than paper checks.

For more on these and other next-gen debit news items, download this month’s Tracker.

How Outreach And Financial Tools Like Prepaid Debit Can Keep Unbanked Consumers In The Financial Loop

The number of unbanked consumers in the U.S. hit a low of 5.4 percent in 2019, the most recent year for which data is available. There were 7 million unbanked Americans, though, and this number has been on the increase due to pandemic-related job losses. In this month’s Feature Story, PYMNTS talked to Sidney King, CEO of Commonwealth National Bank, about why tools like prepaid debit cards can help individuals forge relationships with banks.

Deep Dive: How Alternative Data Can Help Expand Financial Inclusion To The Unbanked

The 7 million American households that lack access to bank accounts often find th at making purchases seeking services in today’s digital-first economy can be a challenge. Even households that have accounts but lack credit histories can find themselves struggling in the modern financial environment, but enabling access to low-cost debit options could go a long way toward boosting their financial health. This month’s Deep Dive takes a closer look at how tapping low-cost debit solutions and alternative data can help community banks and credit unions increase financial inclusion among unbanked and underbanked consumers.

at making purchases seeking services in today’s digital-first economy can be a challenge. Even households that have accounts but lack credit histories can find themselves struggling in the modern financial environment, but enabling access to low-cost debit options could go a long way toward boosting their financial health. This month’s Deep Dive takes a closer look at how tapping low-cost debit solutions and alternative data can help community banks and credit unions increase financial inclusion among unbanked and underbanked consumers.

About The Tracker

The Next-Gen Debit Tracker®, a collaboration between PYMNTS and PULSE, a Discover company, examines consumers’ changing payment behaviors as well as the innovations that are reshaping how they use debit.