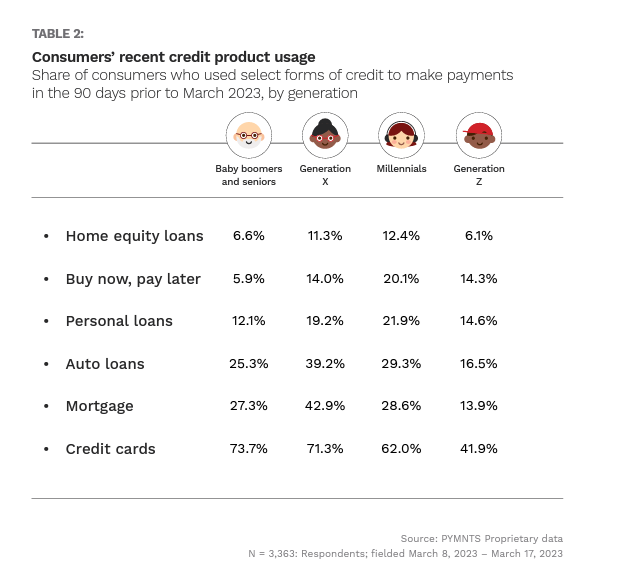

The short-term, interest-free monthly payments offered by buy now, pay later (BNPL) plans are used more by millennials than other generations, as noted in the recent PYMNTS collaboration with Sezzle, “The Credit Economy: How Younger Consumers Make Credit Decisions.” Over 20% of the surveyed age cohort, whose members were born between 1981 and 1996, had used the credit product in the 90 days previous to being surveyed. This represents a more than one-third higher use share than other generations and contributes to millennials’ relatively high credit usage rate overall. Millennials’ respective 12% and 22% rates of home equity and personal loans join BNPL plan use in being utilized most by the generation to represent the highest share of these products used across age demographics.

However, millennials don’t seem to use this outsized share of credit products on discretionary items or frivolous purchases. As a different chart from the same report demonstrates, the generation seems to be focusing its BNPL purchases on necessary items. Millennials have the highest rate of using BNPL for groceries and vehicle maintenance, with 15% and 6% shares, respectively. The age demographic also is most likely to have used BNPL to pay education expenses.

Further supporting the idea that millennials rely on BNPL as a tool for essential purchases are findings in PYMNTS’ collaboration with i2c, “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants.” The report subdivides millennials to add the bridge millennial categorization — the group bridging the millennial and Generation X age cohorts — and that special group exhibited the highest rate of needing to borrow money from family or friends when BNPL was unavailable: 16%. That relatively high share alludes to the urgency of whatever product was being purchased, as generally, more discretionary purchases can often be delayed instead. Consumers in this bind also exhibit a much higher rate of delaying other due payments to complete the purchase in question (at 25%), or turning to cash advances (at 20%), further reinforcing this idea.

This millennial dependence on credit products, in all its forms, may be caused in part by the generation’s financial lifestyle, in which three-quarters live paycheck-to-paycheck. The race to match wages with rising prices has also led 40% of millennials to take on a side hustle to make ends meet. With student loans set to resume in the fall, costing millennials 6.5% overall in spending power, this credit reliance may deepen.

With traditional credit harder to obtain and possibly less appealing as the Federal Reserve continues raising rates, some seek alternative credit and lending options. For millennials, BNPL is providing a key financial lifeline during these turbulent times.