The ability to access credit is a necessity in today’s economy. However, 16% of U.S. consumers find themselves without a credit card. Lack of credit access limits these consumers’ financial flexibility and restricts their access to a valuable lifeline in emergencies. We call these consumers, “credit card outsiders.”

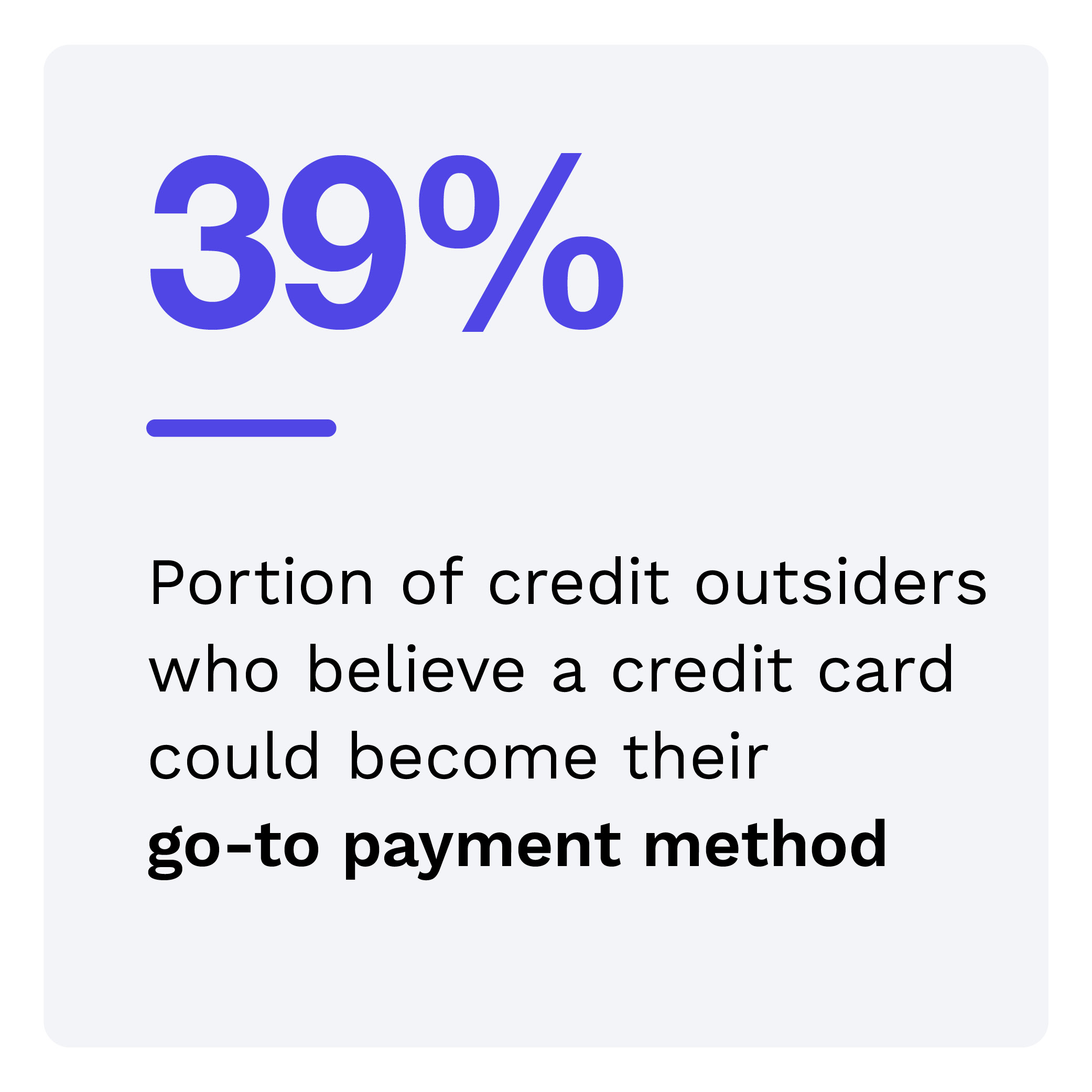

But these consumers are not a monolithic group. Rather, PYMNTS Intelligence finds they fall into four distinct personas: second chancers, credit curious, gone for goods and never-nevers. Nearly half of credit outsiders express a desire to obtain a card in the future.

These are just some of the findings detailed in “Secured Credit Solutions: Assessing Credit Accessibility for Disenfranchised Consumers,” a PYMNTS Intelligence and Atelio collaboration. This report examines why certain consumer groups are unable to access credit cards and how this impacts their financial lifestyles. It draws on insights from a survey of 2,630 U.S. consumers conducted from March 13 to April 2.

Other key findings from the report include:

PYMNTS Intelligence finds that 52% of outsiders once had a credit card, yet three-quarters chose to close their accounts. These consumers cite a variety of personal factors when explaining why they closed their card account. For example, more second chancers faced higher rates of involuntary closure than other outsiders. Understanding the specific challenges different consumer segments face is crucial for card providers and other lenders.

PYMNTS Intelligence finds that 52% of outsiders once had a credit card, yet three-quarters chose to close their accounts. These consumers cite a variety of personal factors when explaining why they closed their card account. For example, more second chancers faced higher rates of involuntary closure than other outsiders. Understanding the specific challenges different consumer segments face is crucial for card providers and other lenders.

Many credit outsiders experience financial strains, with some even struggling with essential expenses. Emergencies are the top financial challenge, emphasizing the critical role that a cushion — even a borrowed cushion like accessible credit — plays in managing unforeseen expenses. Second chancers and gone for goods are almost 50% more likely to struggle to pay for emergencies than other credit outsiders. Providers that position secured credit cards as a lifeline for emergencies could appeal to these outsiders.

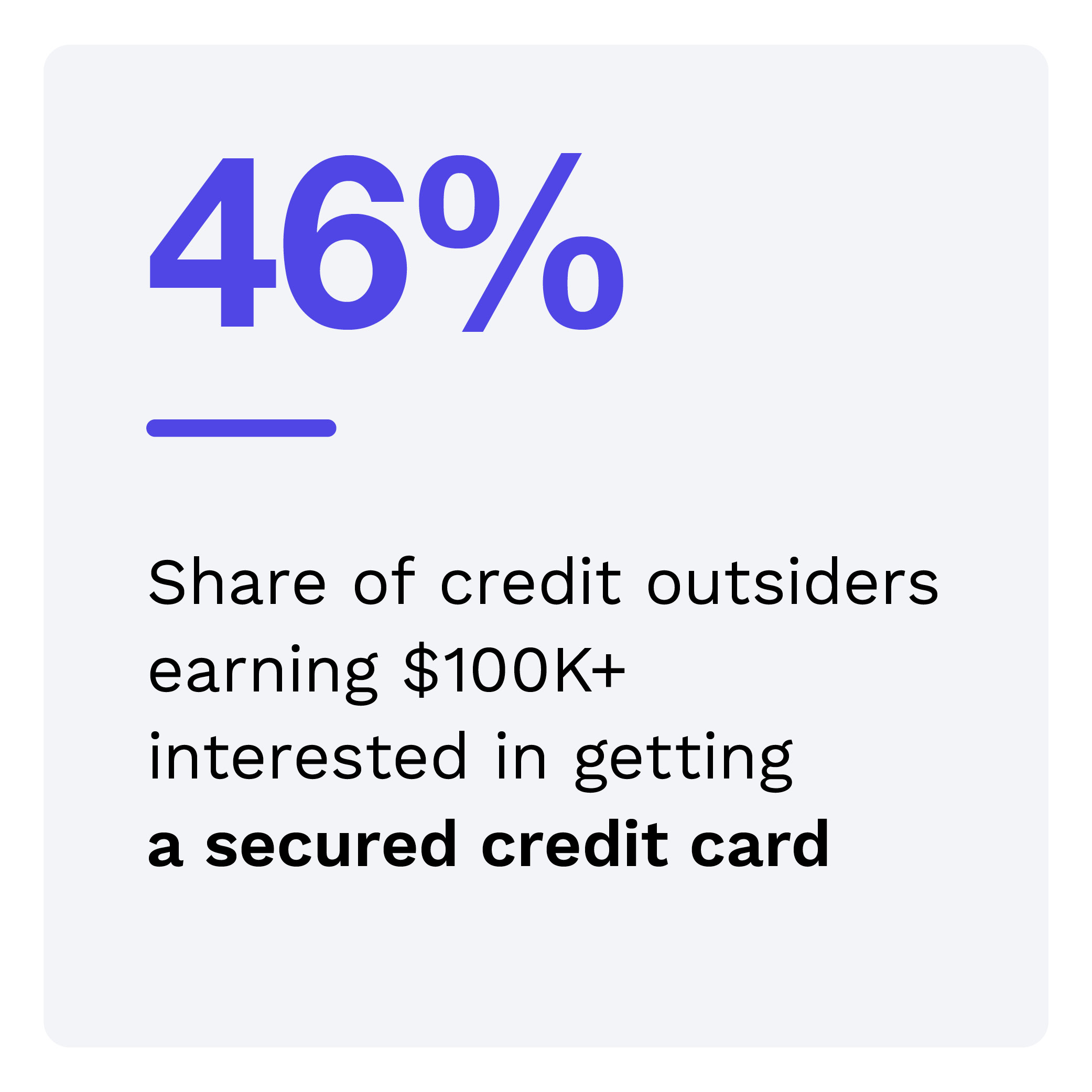

Secured credit cards are a special type of account that appeals to many outsiders. For those who have had issues in the past, a one of these cards could help control spending. For those who have never had a card and are wary, this type of account could introduce credit in a way that is less risky and offers extra security in case of an emergency. In fact, half of credit curious and second chancers are interested in these accounts. In addition, nearly half of those earning more than $100,000 annually report interest in secured cards.

Financial institutions that position secured credit cards as credit building products or financial recovery tools could appeal to credit outsiders. Download the report to learn more about this group of consumers and the secured credit card features they find the most appealing.