Credit unions (CUs) are the underdog in the constant competitive battle among financial institutions (FIs). Established banks can harness far more resources, and digital-native FinTechs have a head start with innovative digital solutions that customers crave. CUs’ traditional advantage over their counterparts — member loyalty — can quickly be whittled away if they do not step up their digital service offerings.

Much of this shift can be attributed to the global changeover to remote banking amid the ongoing pandemic. Branch visits are becoming rarer, and the face-to-face time with FI employees leveraged to earn member loyalty is quickly decreasing. Taking their place are digital services that members can access from the comfort of their homes. These capabilities are quickly swelling beyond the withdrawals, deposits and other basic functions that digital banking has traditionally comprised. FI customers can now access a vast range of banking functionalities, including loan applications, mortgages and new account openings from anywhere, and the FIs that have the most seamless functions are the ones that are pulling ahead.

CU executives are cognizant of this capability gap, however, and are pulling out all the stops to ensure that their institutions can keep their digital edge. Credit Union Innovation: Product Innovation As The Key To Membership Growth, a PYMNTS and PSCU collaboration, outlines CU executives’ long-term innovation plans, how they intend to use new digital services to bolster their appeal to younger generations and the steps they will take to overcome key innovation barriers. We surveyed more than 4,832 United States consumers, 101 CU executives and 51 FinTech executives to determine where CUs were falling behind with digital services, what members require to maintain their loyalty and what digital innovations can have the most impact in keeping CUs competitive with their larger or more agile counterparts.

Key findings from this study include:

Key findings from this study include:

• Demographic shifts are putting pressure on CUs and other FIs, with younger generations placing a greater emphasis on digital services. Fifteen percent of Generation Z consumers said they are dissatisfied or only slightly satisfied with their current FIs, the highest share of any generation surveyed. These consumers had various reasons for their dissatisfaction: 40% cited high costs, 21% complained about the poor quality of mobile banking services and 21% said it was difficult to use bill pay services.

• CUs are growing more cognizant of the causes of member dissatisfaction and are becoming more aggressive when it comes to new product development and introduction. Nineteen percent of CUs are now classified as “early launchers,” defined as institutions that innovate new products before their rivals. The proportion of early launcher CUs stood at just 12% last year, an increase of 58%.  Another 36% of CUs are classified as “quick followers,” up from 28% of CUs in 2018. The combination of early launchers and quick followers now comprises half of all CUs, indicating an industry shift in the early development and launch of new digital banking products.

Another 36% of CUs are classified as “quick followers,” up from 28% of CUs in 2018. The combination of early launchers and quick followers now comprises half of all CUs, indicating an industry shift in the early development and launch of new digital banking products.

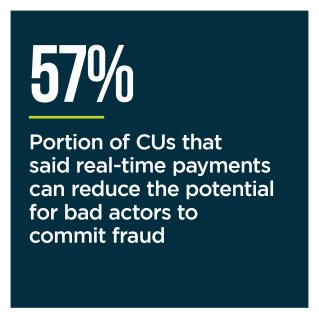

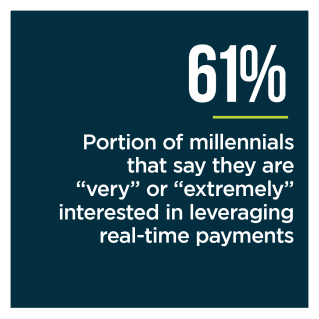

• Real-time payments are of particular interest to CUs’ important demographics: millennials and bridge millennials. Sixty-one percent of millennials and 59% of bridge millennials are highly interested in real-time payments for various reasons. Twenty-three percent of consumers said real-time payments are easy to use and convenient, and 22% said they appreciate the instant availability of funds. Another 14% said that real-time payments could help them track their financial situation.

To learn more about how CUs are developing new digital services to help drive retention, download the playbook.