When it comes to payments fraud, the Federal Reserve actually splits the crime into two categories: authorized and unauthorized fraud.

While unauthorized fraud — which involves fraudsters initiating or redirecting bogus payments from legitimate accounts — might be the type that first comes to mind when thinking of fraud, authorized fraud is nearly as pervasive.

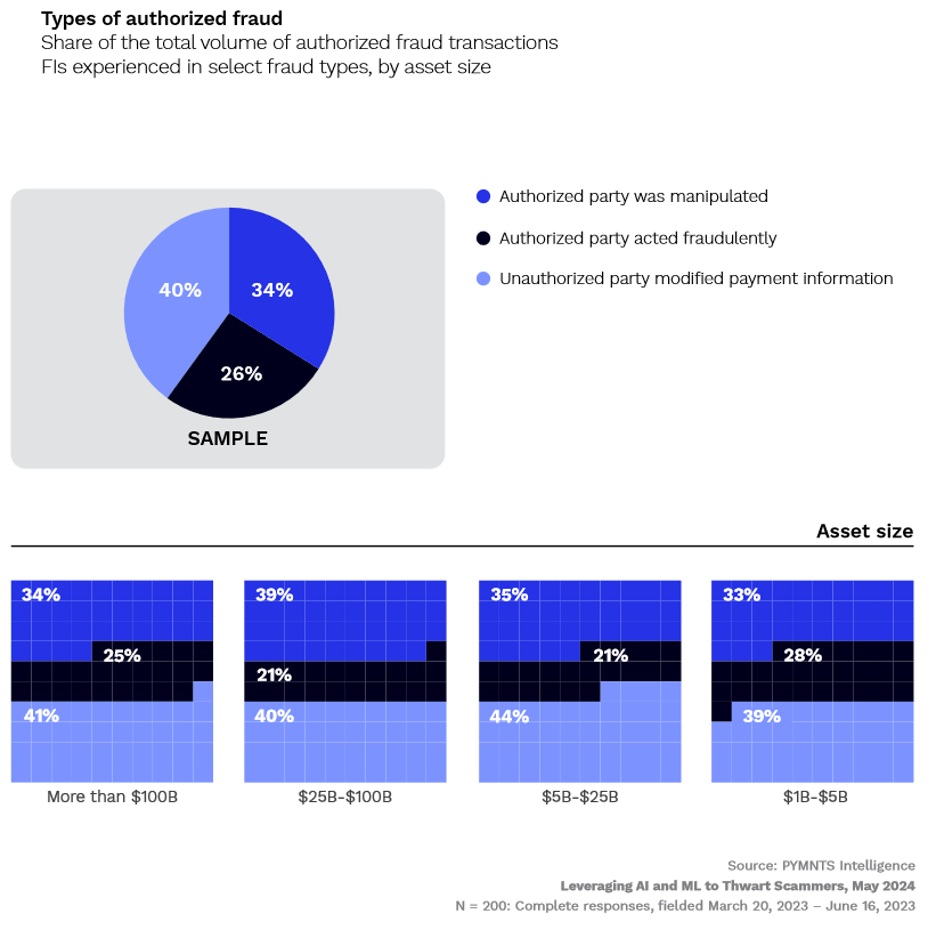

Authorized fraud pertains to schemes where account holders unwittingly initiate or approve payments to bad actors, usually because they have been manipulated or deceived into believing the transactions are warranted.

As PYMNTS Intelligence reported in “Leveraging AI and ML to Thwart Scammers,” a study we created in a collaboration with Hawk, 43% of all fraudulent transactions that financial institutions (FIs) process are, in fact, authorized fraud.

Even though 4 in 10 FIs are victimized by some kind of authorized fraud, we found overall that the losses are less severe than those brought on other forms of fraud. Authorized fraud accounts for just 37% of the total money FIs lose to fraudsters; however, the share of total dollars lost increases with FI size, accounting for 44% of fraud losses for FIs with more than $100 billion in assets under management (AUM).

The most common type of authorized fraud occurs when fraudsters modify payment information or instructions, redirecting funds into their own coffers. As the accompanying figure illustrates, this type of fraud accounts for 40% of all authorized fraudulent payments.

The second most common type of authorized fraud, representing 34% of occurrences, are scams where a fraudster manipulates or deceives an authorized party into making a payment. Even though they come in second place, these scams represent 14% of all fraudulent transactions for FIs that manage $5 billion or more in assets.

These types of swindles are particularly concerning to FIs because — in addition to triggering losses — they negatively impact customer satisfaction and retention. Customers expect their FIs to protect them from fraud, so naturally when those customers learn that their institutions permitted the fraudulent transactions, it undermines trust — and customer churn is a common outcome.

PYMNTS Intelligence data reveals that 53% of the scams FIs report are product or services fraud, where users purchase goods and services that are never provided; the other 47%, meanwhile, are relationship or trust fraud, where customers are manipulated by a fraudster who eventually requests funds. Product or services fraud is the most common for the smallest FIs, while relationship fraud is most common for FIs with between $5 billion and $25 billion in assets.

Although authorized fraudulent transactions may cost slightly less than unauthorized fraud, both forms of fraud can erode customer trust. But as the data illustrates in “Leveraging AI and ML to Thwart Scammers,” FIs can mitigate this damage by exploring advanced fraud prevention ML or AI tools, which have proven to be successful in protecting both FIs’ bottom line and their customers’ confidence.