Digital-first consumers increasingly power today’s economy, which makes money mobility a top requirement for any financial services provider. Prospective customers expect this ability, and the need to meet this growing demand is especially strong for burgeoning FinTechs set on winning consumers away from traditional banks.

The average FinTech account issuer barely earns a passing grade on money mobility, with an average Index score of 53.5 out of 100, according to PYMNTS’ data.  In practice, this means that FinTech account issuers have many opportunities to improve their customers’ experience — and, in turn, better engage and retain consumers.

In practice, this means that FinTech account issuers have many opportunities to improve their customers’ experience — and, in turn, better engage and retain consumers.

For account holders, money mobility means more than easily sending payments by moving money out of accounts. It also means instant access to funds deposited into their account from any payment method. If FinTech issuers want consumers to feel confident using their offerings in lieu of a bank’s, they must offer all the services consumers expect from traditional issuers.

These findings are part of the “2023 Money Mobility Index,” a PYMNTS and Ingo Money collaboration. The Index is based on two surveys. The first was a census-balanced survey of 3,633 consumers across the United States, investigating what consumers want and expect from the nonbank financial services firms from which they transact and was conducted between June 9, 2022, and June 23, 2022. The second survey was conducted between Aug. 3, 2022, and Aug. 25, 2022, and reached 200 executives from FinTechs across the U.S. to reveal the level of customer satisfaction with the money movement capabilities they provide.

Other key findings from the study include the following:

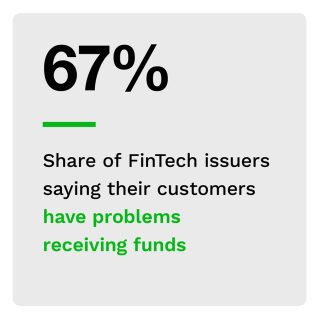

• Account holders are 51% likelier to report issues receiving funds than for sending them out.

Sixty-seven percent of issuers say their account holders experience difficulties when they receive funds into their accounts, but just 45% say their account holders experience similar difficulties sending money out of their accounts. The most likely explanation is simple: account holders want their money as fast and with as few hiccups as possible.

• Top-performing issuers have high customer satisfaction for sending and receiving money, yet security remains a challenge.

At least 67% of top performers say their customers have no problems using select money-out features, yet just 23% of bottom performers can say the same. Similarly, 80% of all bottom-performing firms’ customers experienced issues receiving funds from individuals, exceeding the 67% of top-performing issuers’ customers who had the same issues.

As for security, even top-performing issuers have room to improve: 60% of issuers report that customers depositing funds faced problems using security features, as did 33% of customers withdrawing funds.

As for security, even top-performing issuers have room to improve: 60% of issuers report that customers depositing funds faced problems using security features, as did 33% of customers withdrawing funds.

• Instant payments are particularly valuable: The more instant payment options issuers provide, the greater money mobility customers have, and the more customers will use their accounts.

Payment choice is critical to winning over and keeping customers, but not all payment methods are created equal as far as account holders are concerned. Instant payment methods are key. Our researchers found that FinTechs offering multiple instant payment methods provide smoother experiences and, as a result, earn higher Index scores. Issuers that offer six or more instant payment methods, either for receiving or sending money, earn an average Index score of 59.5, while those that offer two or fewer instant methods earn an average score of just 50.6.

To learn more about how FinTechs can improve customer satisfaction and experience when moving money in and out of accounts, download the report.