Black Friday is in the rearview mirror, the gifts are on their way, if they haven’t been delivered to doorsteps already.

And as the dust settles, we can gain a clearer picture of just how consumers’ payments preferences are shifting, amid the economic uncertainty wrought by the ongoing pandemic, and by rising interest rates.

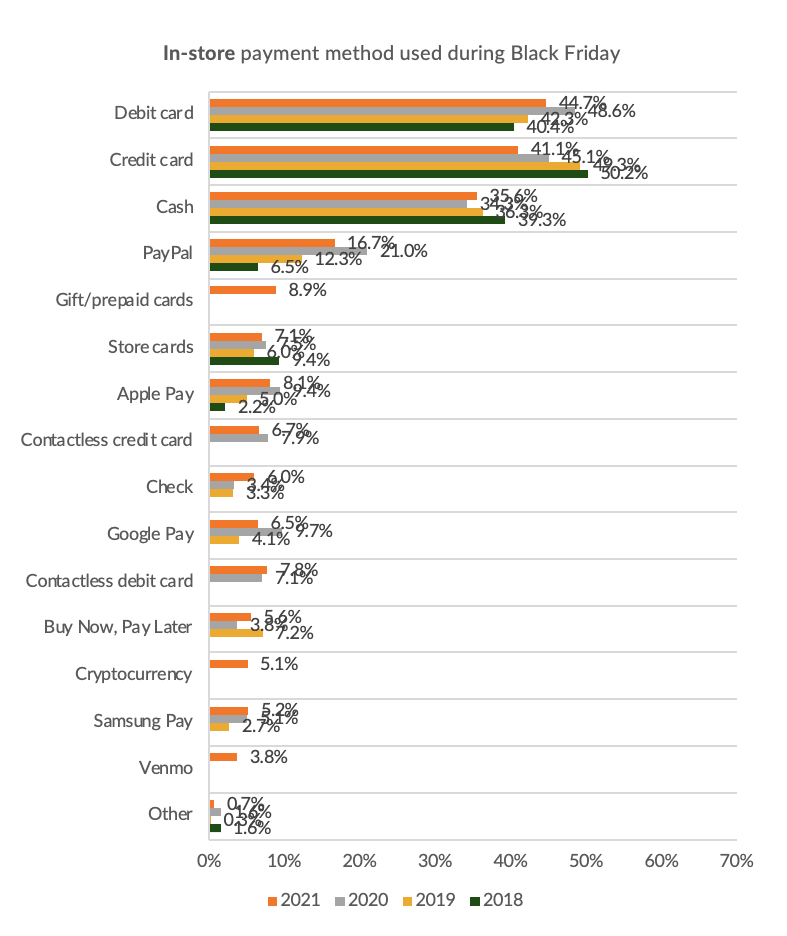

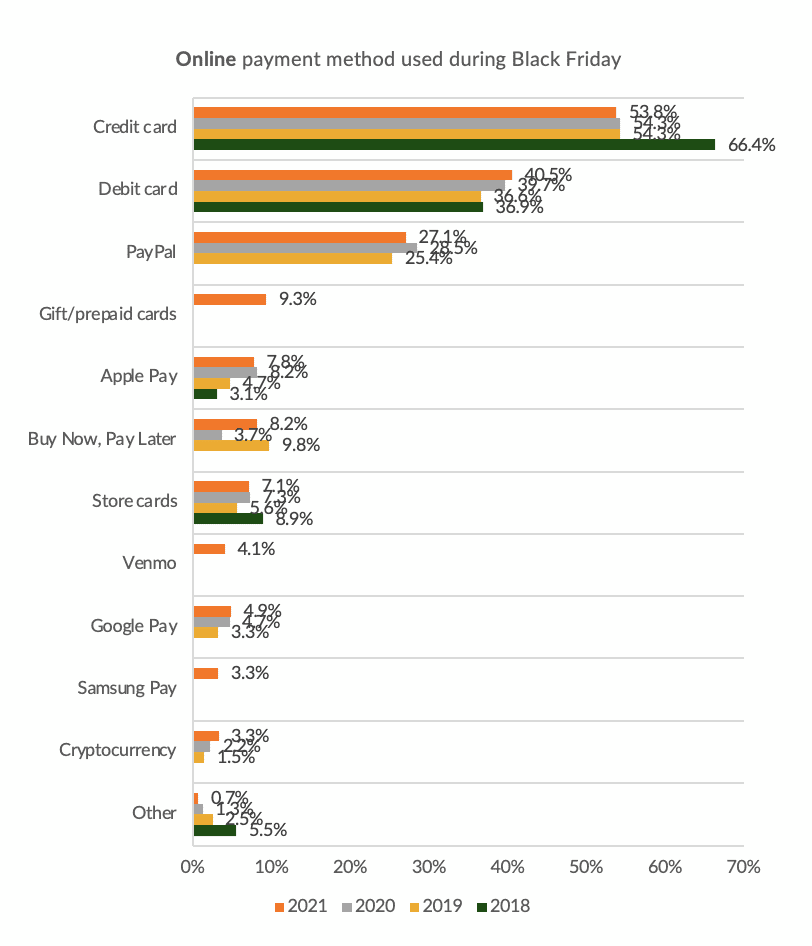

We’ve documented in past articles details on how debit and credit were, and are, being used in-store and online. PYMNTS surveys of more than 2,000 consumers found that, by and large, individuals opted to spend the cash on hand rather than load up the credit cards.

Source: PYMNTS Data

But the data also show the continued embrace of buy now, pay later (BNPL) options at the point of checkout — whether at the register (that would be at brick-and-mortar locations, of course) or, where applicable, through various “virtual” carts.

At a high level, we note that BNPL still represents a relatively small piece of the payments “pie.” Only a low to mid single-digit percentage point segment of all consumers queried said they’d used BNPL for their Black Friday purchases. In store, as evidenced in the chart above, 5.6% of consumers used the option this year, up significantly from 3.6% in 2020.

Similarly, in the chart below, detailing the activity online, we see that BNPL captured an 8.9% share of payment activity in 2021, up from 3.7% last year. It’s worth pointing out that the recent data seems to represent a “rebound,” where 2020 seemed to be a nadir for BNPL (certainly as compared to pre-pandemic levels), and that would seem to make sense, given the pivot last year to debit as the economic headwinds were in full force.

Source: PYMNTS Data

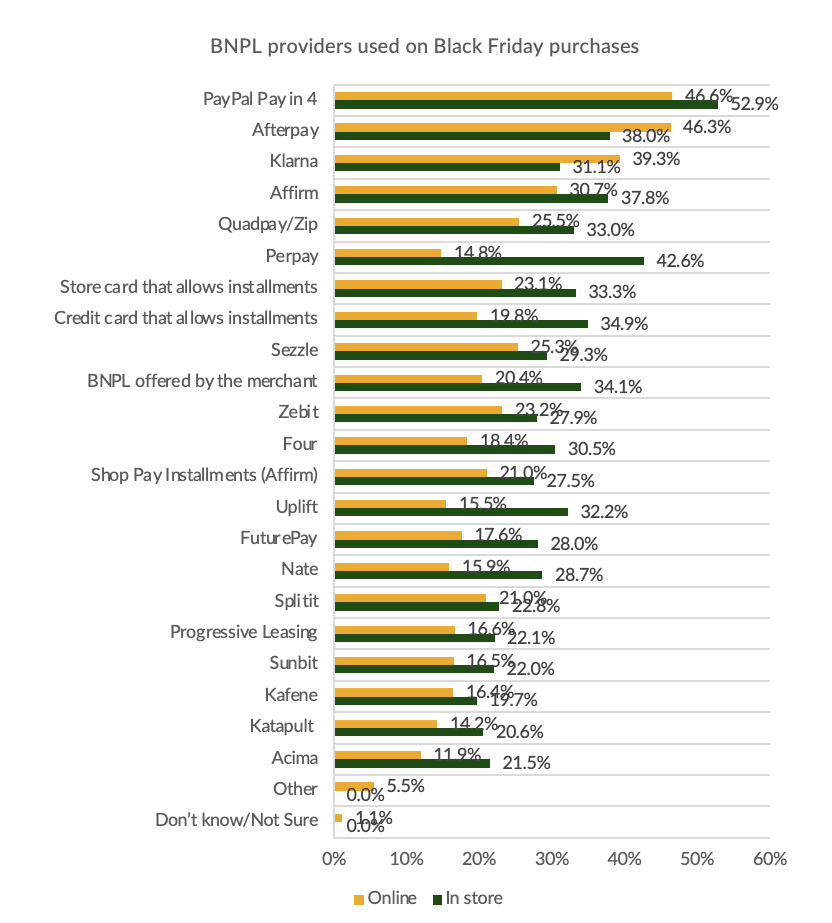

One note regarding the data points themselves: Our granular insight into just which providers consumers used is based off a fairly small sample, with roughly 35 respondents for in-store shopping and 65 for online purchases. But the preferences seem clearly indicated. By and large, most providers saw more “use” instore, at the actual, physical point of sale. Two notable exceptions were Afterpay and Klarna, where online purchases dominated by several percentage points. Recent data from Afterpay underscore the growing popularity of BNPL and online purchases using BNPL.

Source: PYMNTS Data

As reported Wednesday (Dec. 1), Afterpay said that BNPL spending in the U.S. has increased 230% in the past year, with a 34% increase this holiday season compared to last year. Afterpay said that there has been a 30% increase year over year of people using its BNPL offerings,

Read also: Afterpay: BNPL Purchases up 34% From Last Year

BNPL, at least according to the most recent data points, is gaining ground in consumers’ minds as a useful payment option, and with low penetration (again, it’s in the single digits), there’s room to grow. But much depends, of course, on how and when (perhaps it’s not a case of if) the regulatory landscape evolves — and whether providers might face restrictions in yet-unforeseen ways.

As related in this space recently, BNPL is to be regulated by the U.K. Financial Conduct Authority (FCA) following a review that lasted several months. In looking at the largely unregulated sector, the FCA recommended that, among other initiatives, there needs to be the “secure provision of debt advice,” especially against the landscape where more than 42 million people used consumer credit in 2019.

In the U.S., the Consumer Financial Protection Bureau (CFPB) said this year, too, that “BNPL may seem straightforward and convenient; however, you should consider a few things before selecting this option to make a purchase.” The CFPB said that BNPL loans currently lack the consumer protections that apply to credit cards.

We’ll see if the toeholds made by BNPL, evidenced in heady growth through the holiday season (as just one moment in time) will be sustainable.