In a credit-based economy like the United States, credit scores play a crucial role in determining access to credit and financial stability. This poses a considerable challenge for millions of individuals with lower credit scores, significantly impacting their ability to manage finances effectively.

According to a survey conducted by PYMNTS Intelligence, nearly 30% of consumers have credit scores of 650 or less, which denies them access to credit products. This consists of individuals in the deep subprime category — those with credit scores of 579 or lower — who are twice as likely as the average consumer to have trouble paying their monthly bills or affording essential items.

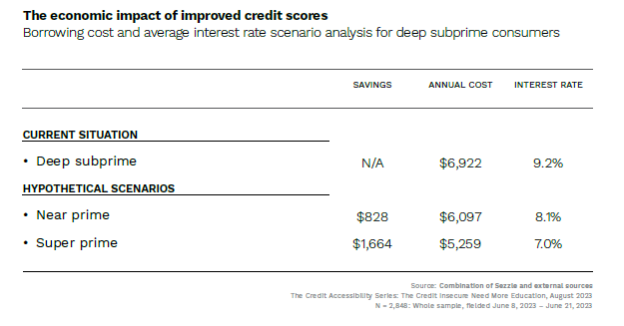

Additionally, consumers in this category have $75,000 in outstanding debt at an interest rate of 9.2%, resulting in $6,900 in annual interest payments. Consequently, they allocate a significant portion of their disposable income toward repaying these higher-interest loans — a financial burden they can significantly ease by improving their credit scores, the study found.

For instance, improving their scores to the near prime range of 620 to 659 would decrease interest payments to 11.8% of their disposable income and increase their borrowing capacity by 68%, allowing them to finance an additional $44,000 worth of purchases.

Additionally, attaining a super prime score of 720 or above could decrease their interest payments to $5,300 annually — an amount equating to roughly 10% of their disposable income. Moreover, achieving this score would triple their borrowing capacity, enabling them to secure an additional $130,000 in financing.

The survey further highlights the correlation between credit scores and credit knowledge. Most consumers with low credit scores don’t know how to improve their credit status and a mere 27% of consumers are aware that using loan products like buy now, pay later (BNPL), which have no or very low interest, could also be used to enhance their credit scores. This creates an opportunity for financial product vendors to find innovative ways to reach these consumers and provide them with the necessary credit education.

Overall, improving credit scores can have a significant positive impact on the financial well-being of credit insecure consumers, particularly those in the deep subprime category. By raising their scores, these consumers can access lower interest rates, increase their borrowing capacity, and improve their overall financial stability.

However, there is a need for increased credit education; financial institutions and credit product providers should explore innovative ways to reach these consumers with the necessary tools and information. By offering resources such as online credit education courses and personalized credit counseling, these institutions can empower deep subprime consumers to enhance their credit scores and financial futures.