Life continues to be more expensive for everyone. Data shows that United States consumers in urban centers, in particular, are feeling the financial crunch. PYMNTS’ research finds that 61% of consumers lived paycheck to paycheck in April 2023, a share similar to last year.

Consumers in urban areas are more likely to live paycheck to paycheck than others, suggesting a connection to cost of living. Still, the wealthiest consumers comprise a growing portion of the paycheck-to-paycheck cohort. The share of consumers annually earning more than $100,000 who live paycheck to paycheck increased 7 percentage points from April 2022.

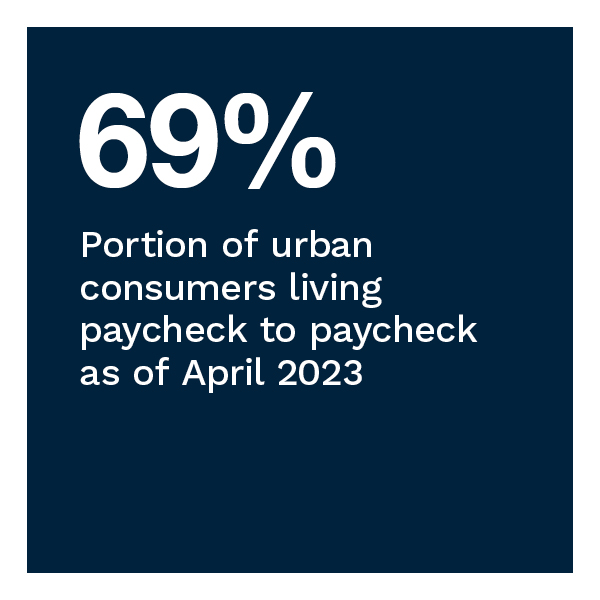

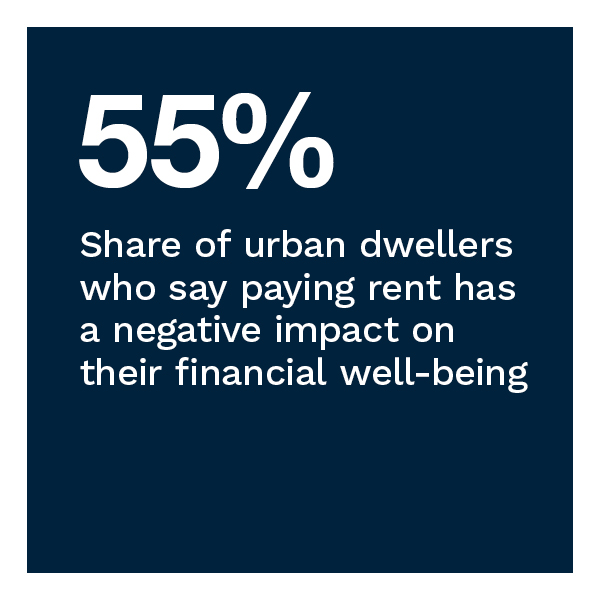

High-income consumers are particularly likely to live in urban areas. Having higher incomes does not prevent nearly 70% of urban dwellers from living paycheck to paycheck. More than half of urban dwellers report paying rent negatively impacts their financial well-being. Supporting dependent relatives and discretionary spending are the top reasons cited for living paycheck to paycheck.

These are some of the findings detailed in “New Reality Check: The Paycheck-to-Paycheck Report,” a collaboration with LendingClub. The Regional Divide Edition examines why consumers in different areas of the U.S. live paycheck to paycheck and identifies their financial stressors. This edition draws on insights from a survey of 3,652 U.S. consumers conducted from April 3 to April 17, as well as an analysis of other economic data.

More key findings from the study include the following:

PYMNTS’ research finds that nearly three-quarters of urban consumers live paycheck to paycheck across all regions except the South. Just 62% of urban dwellers in Southern cities, such as Memphis and New Orleans, live paycheck to paycheck. These urban dwellers are the most likely to cite insufficient income as the chief driver of their financial distress. Thirty-two percent report their paycheck barely covers their bills. Having significant debts to repay is the second most popular reason for financial distress among Southern urban dwellers.

Credit product usage is higher among urban consumers. Eighty-three percent of urban consumers in all regions have made at least one credit product-related payment in the last 90 days. Urban dwellers in the Northeast and the West are the most likely to have made a credit product payment, at 88% and 87%, respectively.

The exception, unsurprisingly, is auto loans, where suburban and rural consumers take the lead. Among urban dwellers, those in the West are the most likely to have made an auto loan payment in the last 90 days. Western urbanites are also significantly more likely to have made a personal loan payment than those in other regions.

Eighty percent of consumers who have noticed price increases believe their wages have not increased to at least match inflation. Although urban consumers are the least likely to say that wage increases did not at least match inflation, 71% reported that wage increases were less than the rate of inflation. In comparison, 84% of those living in suburban and rural areas believe wage increases did not at least match inflation. Urban consumers are also more optimistic about their job prospects than suburban or rural consumers.

Download the report to learn more about how ongoing inflation impacts consumers living paycheck to paycheck in different U.S. regions.