Card-issuing banks offering payment advice to clients may benefit from decreased delinquencies and higher long-term customer retention.

Data suggests that consumers are increasingly reaching for their credit cards to handle payments — perhaps not surprising, as nearly two-thirds of consumers continue to live paycheck-to-paycheck — and earnings reports across the industry suggest that a sizable portion of these cardholders may be biting off debt that they cannot chew.

American Express’ earnings report last week for the last quarter of 2022 reflected that credit cards continue to be a preferred payment method across age demographics. Amex customers overall charged 15% more than they did a year ago, and their loans-past-due and write-off rates are also increasing, albeit still well below pre-pandemic levels.

Wells Fargo saw new card accounts rise by 31% in 2022 and credit card point of sale (POS) sales rise by 17%. However, the bank’s card loans over 30 days late rose as well during the same period, as did consumer net loan charge-offs. This implies that consumers are using their cards more yet are also increasingly having trouble paying these debts back. Capital One observed similar growth, although the bank’s provision for credit losses was up $1.4 billion year-over-year, compared to $384 million the previous year.

J.P. Morgan also reported that its credit and debit sales volume were up 9%, though net charge-offs in the segment were $845 million, representing a $166 million increase over the previous quarter. It is clear that some consumers are struggling to stay afloat, despite credits’ increased use: A St. Louis Federal Reserve commentary highlighted that delinquency rates for all banks in the third quarter of 2022 reached 2.1%, from 1.6% in Q3 2021.

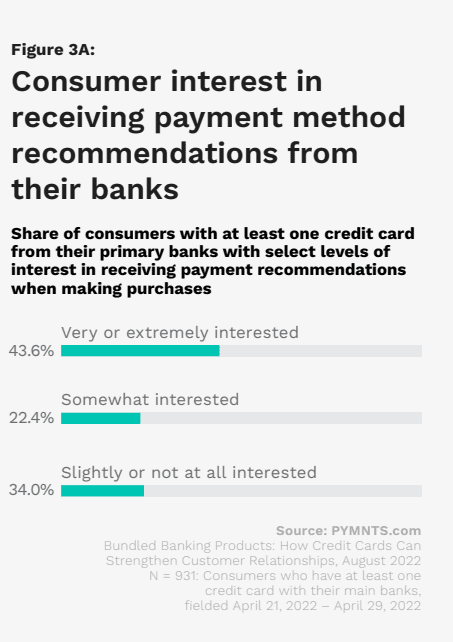

The PYMNTS/Amount collaboration, “Bundled Banking Products: How Credit Cards Secure Customer Loyalty,” finds that this increased card usage comes with increased consumer interest in managing this debt.

Card-issuing primary banks have a multi-layered opportunity by offering features such as payment method recommendations to their customers. As personal debt rose to a seasonally adjusted 7.1% in November and signs point to consumers straining to manage debt, this kind of guidance could help account holders optimize their payment options, improving their financial health. Generally based on customer transaction data, payment recommendation feature software runs that data through algorithms to create personalized advice, which can include identifying the best card or deal for a specific merchant as well as suggesting methods that may be beneficial but unknown to the consumer, such as interest-free BNPL options. These programs may be particularly well-received by paycheck-to-paycheck customers, as this consumer segment is three times more likely than others to revolve their monthly debt and carry higher balances.

For primary banks, leveraging transaction data to offer payment recommendations to their card-issued clients has a real chance of increasing loyalty and retention. This is especially true for banks’ younger clients, as data finds that both millennials and members of Generation Z indicate a willingness to opt into and follow wealth-building advice. Winning over these age groups as they seek trusted sources to start their financial journeys could be essential to future success.

By solidifying ties with customers and possibly reducing delinquencies through optimization, payment method recommendation features and similar programs are a near win-win for card-issuing primary banks. As consumers keep using more and more credit and seek help to stay afloat in unsteady conditions, FIs that step in and roll recommendations out quickly will be best positioned to earn their affinity over the long haul.