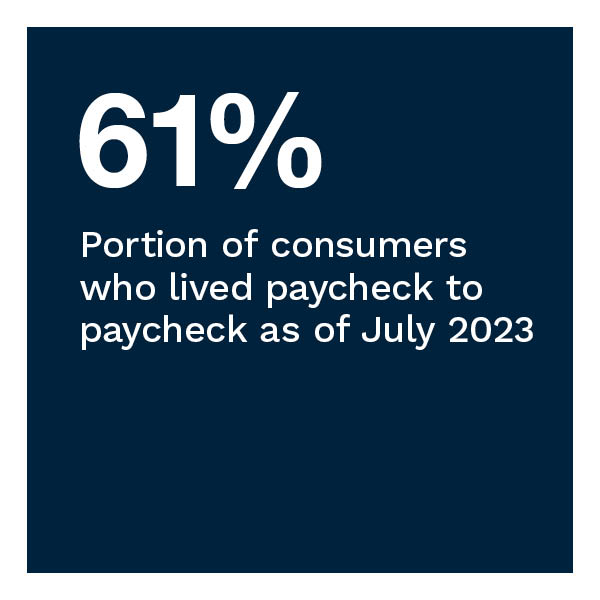

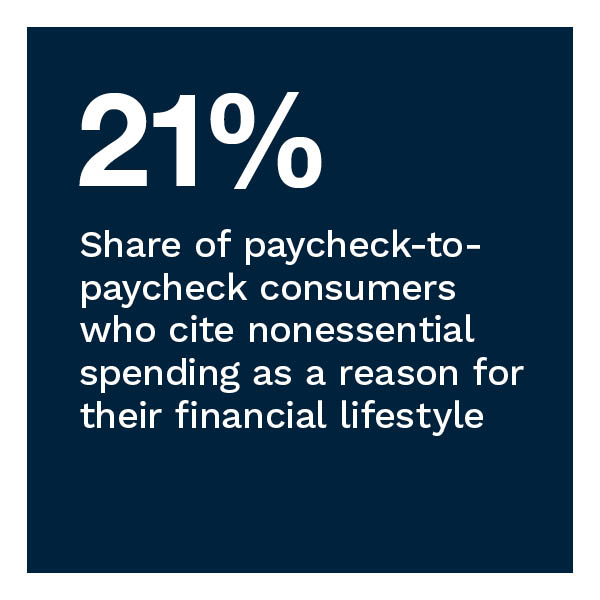

Inflationary pressures have yet to abate fully, making it necessary for many United States consumers to adjust their lifestyles to live within their means. Even as consumers work hard to manage budgets and put aside savings, 61% lived paycheck to paycheck as of July 2023, with 21% struggling to pay monthly bills. How consumers manage essential and nonessential spending is a crucial gauge of financial standing.

PYMNTS’ research finds that according to 21% of paycheck-to-paycheck consumers, nonessential spending is one reason for their financial lifestyle, with 10% saying it is their top reason for living paycheck to paycheck. Even so, two-thirds of paycheck-to-paycheck consumers say they include discretionary items when shopping at least some of the time. This factor is significant as it signifies how consumers, despite financial challenges and tighter budgets, indulge in nonessential spending when possible.

These are just some of the findings detailed in this edition of “New Reality Check: The Paycheck-to-Paycheck Report,” a PYMNTS and LendingClub collaboration. The Nonessential Spending Deep Dive Edition examines the impact of nonessential spending on consumers’ ability to manage expenses and put aside savings. The series draws on insights from a survey of 3,443 U.S. consumers conducted from July 5 to July 20, as well as an analysis of other economic data.

Key findings from the report include:

PYMNTS’ research shows that engagement with most service categories shows little difference across financial lifestyles. For instance, among consumers living paycheck to paycheck and struggling to pay bills, 43% engage with leisure or travel services — not too different from the 50% of those living paycheck to paycheck without difficulty who engage with those same services. Whether living paycheck to paycheck or not, consumers remain engaged with dining out, retail purchases and household digital services. This lack of differentiation suggests that when consumers need to adjust their budgets, they tend to reduce their spending in the same service categories.

Consumers engaging in indulgent spending in at least three of the 30 proposed product and service categories have savings balances 26% higher on average than those who do not engage in indulgent spending. In contrast, 36% of Gen Z consumers say they engage in indulgent spending, and those who indulge have similar average savings as other members of their generation without indulgent spending. Among paycheck-to-paycheck consumers, just one-quarter spend on “nice-to-have” items, with those who indulge reporting slightly more savings than those who do not.

While most service categories reveal few differences in engagement across financial lifestyles overall, our study finds a correlation between financial standing and what specific services consumers allow themselves to indulge in. Paycheck-to-paycheck consumers, for instance, are more likely to cite indulgent spending at QSRs than those not living paycheck to paycheck, at 27% and 20%, respectively. Streaming services represent another area where financially struggling consumers cite somewhat indulgent spending compared to other consumers.

Struggling consumers continue to find ways to manage their budgets to make ends meet in today’s financial environment, but they need to be cautious about their discretionary spending. Download the report to learn more about the impacts of nonessential spending on U.S. consumers living paycheck to paycheck.