Ubiquity is what we all want in a rewards program.

Ubiquity allows consumers to redeem rewards for the value — the goods and services — they prefer, as their “convertibility” carries across various use cases.

We may all be familiar with the statement credits, with miles that are redeemable only on a certain airline. And some folks reading this article may be able to recall the catalogs that offered a menu of options for reward redemptions. Cash back options stretch back to the mid 1980s.

The recent news that American Express cash-back cardholders can now spend their Reward Dollars on Amazon helps forge a bit more of the path towards ubiquity. As PYMNTS reported Monday (Nov. 20), a single Reward Dollar equals $1 on Amazon’s website or app. Cardholders can link their eligible American Express card to their Amazon account and then select Reward Dollars as the payment method at checkout, and the rewards dollars help defray, or cover, the cost of the item being bought on Amazon.

For both companies, we note, there’s a positive ripple effect. American Express ostensibly keeps members spending with the cards they already have on hand, with the fungibility of its rewards, and it may be the case that individuals who shop frequently on Amazon might be tempted to sign up for Amex cards.

For Amazon, there’s the lure of gaining younger consumers, and bringing more Millennials and Generation Z individuals into its ecosystem. As we noted in our recent coverage of Amex’s earnings, Millennials and Gen Z consumers accounted for more than 60% of all new consumer account acquisitions globally in the quarter. Millennial and Generation Z cohorts’ spending continues to be robust, up by double digits and represented roughly a third of total consumer-related spending.

Separate PYMNTS Intelligence data underscore the benefits of spurring spending among younger demographics: On average, baby boomers and seniors dedicated $477 to credit card purchases in the last 90 days, almost half that of Generation X and a third of millennials.

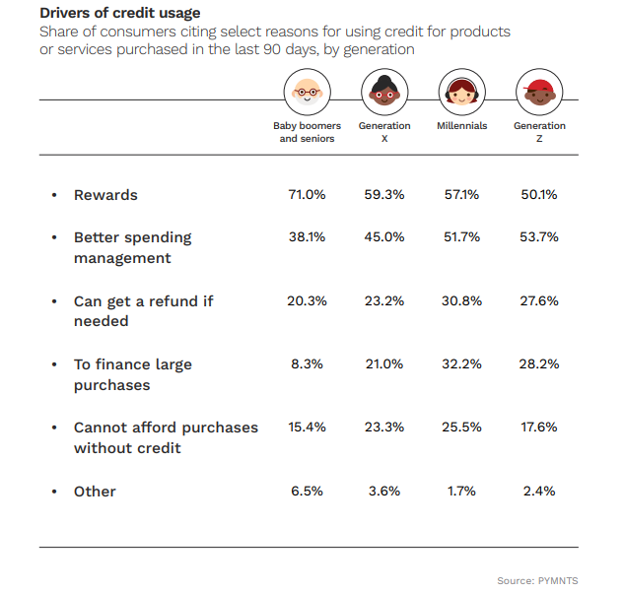

But as seen in the chart below, the potential is there to get older generations to spend more. A majority of consumers — no matter what age group — cite rewards as a top reason for credit usage. But boomers and seniors lead the pack, so a strong rewards program, and as noted above, a far-reaching one, may help incentivize them to spend via their cards, too.

The rewards-as-currency shift has been evident in recent months as firms move beyond the confines of credit card statements.

As reported here earlier in the month, Engage People Chief Technology Officer Len Covello told PYMNTS that “what we’ve seen over the past few years is that loyalty programs have tried to leverage personalization,” moving beyond the “blindsiding email blasts that go out to everyone, where the click-through rate might be quite low,” he said.

Paying with points is proving to be especially valuable in a macroeconomic environment where many everyday essentials are more expensive than has been seen in decades, Covello said.

“You want that loyalty transaction to happen specifically when you’re interacting [with a merchant] in your day-to-day life,” he said.